The Iran war has triggered a sharp surge in global gas prices, particularly in Europe and Asia. However, Henry Hub has responded more modestly, reflecting its domestic focus.

This note explores the divergence, key constraints limiting U.S. gas prices, and what the current setup implies for Henry Hub in the months ahead.

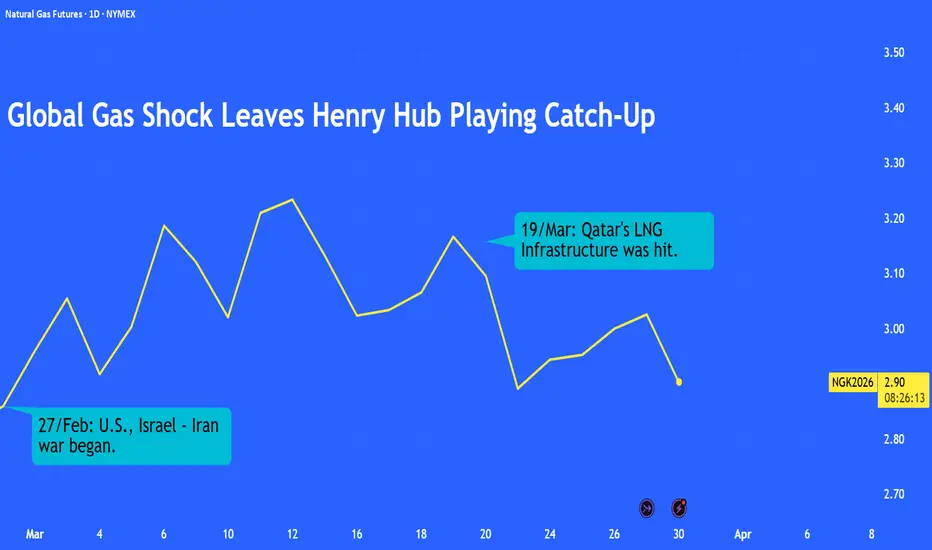

GLOBAL SHOCK HITS HARD ABROAD WHILE U.S. GAS STAYS GROUNDED

The Iran war, which began on 28/Feb, triggered a sharp repricing across global energy markets, with natural gas seeing one of the strongest reactions.

Disruptions to the Strait of Hormuz, through which roughly 20% of global LNG flows, significantly tightened global supply. Additionally, attacks on Qatar’s Ras Laffan Industrial City alone have taken out about 17% of LNG capacity, with repairs expected to take three to five years.

As a result, global gas prices surged, particularly in Europe (TTF) and Asia (JKM), as markets priced in both immediate disruptions and longer-term supply losses.

The sharp rise in TTF and JKM prices reflects both immediate supply disruptions and potential multi-year capacity losses.

In contrast, Henry Hub has seen a much more muted response. Prices have moved higher, but only modestly.

This divergence highlights a key structural feature of the gas market: Henry Hub remains largely driven by domestic fundamentals.

The outperformance of the TTF can be attributed to several factors:

The chart below shows EU gas storage levels relative to the 5-year average, currently sitting near the lower end of the range.

Source: Swiss Federal Office of Energy

Overall, while Henry Hub has moved in the same direction, the magnitude has been far smaller, reinforcing that U.S. gas prices remain largely insulated from global dislocations.

DOMESTIC CONSTRAINTS: WHY HENRY HUB CANNOT FULLY REPRICE

Despite tightening global LNG markets, Henry Hub’s upside remains limited by domestic fundamentals.

U.S. supply remains strong, and inventories are still at comfortable levels. At the same time, LNG export capacity is already running at full capacity, leaving little room to increase volumes, even as global prices surge.

Source: EIA Natural Gas Storage Data

While a larger-than-expected withdrawal of 132 Bcf (week ending 27/Feb) reflected strong winter demand, overall storage levels have not come under significant stress since the war began.

Source: EIA and Investing.com

On the supply side, U.S. production remains robust. Output has averaged around 109.6 Bcf/d in March, while 2025 production hit a record 118.5 Bcf/d. Production is expected to grow further in 2026, reinforcing the strength of domestic supply.

According to LSEG data, U.S. LNG exports are currently running at approximately 19 Bcf/d, with export terminals operating near full capacity and little spare capacity available.

This creates a key constraint; despite strong global demand, the U.S. cannot significantly increase exports in the short term. As a result, even though global arbitrage opportunities have widened sharply, at times exceeding 200%, Henry Hub has not seen a comparable price surge.

Looking ahead, supply growth may also face delays. At CERAWeek, the CEO of Freeport LNG noted that geopolitical disruptions could slow new project timelines due to constraints in materials, labour, and supply chains.

KEY DRIVERS IN THE MONTHS AHEAD

Looking ahead, Henry Hub is likely to remain supported but not fully re-rated in line with global benchmarks.

On the bullish side, persistent global LNG supply disruptions, particularly from Qatar, are expected to sustain strong demand for U.S. exports, providing a structural floor to prices

However, prices will be anchored to U.S.-centric factors such as:

Weather forecasts will play a key role in Henry Hub’s price action in the coming months. As winter draws to a close in March, prices often soften amid lower heating demand and rising storage injections, before finding support again in the summer (June -August) due to air-conditioning load.

OPTIONS MARKET SIGNALS LIMITED DOWNSIDE WITH UPSIDE TAIL RISK

Options positioning in Henry Hub shows a bullish setup, with a put-call ratio of 0.67.

Source: CME QuikStrike

However, the structure of positioning is more telling. There is meaningful open interest in far out-of-the-money calls (above USD 4), indicating the market is pricing upside tail risk, a scenario where prices could spike if supply disruptions worsen.

At the same time, put positioning is concentrated close to current levels, suggesting that the market sees limited downside from here.

Source: CME QuikStrike

In short, the options market is not aggressively bullish, but it is clearly skewed toward asymmetric upside risk, with downside seen as relatively contained.

HISTORICAL EXAMPLE

The Russia-Ukraine War created a similar backdrop, where disruptions to global gas flows had an immediate and outsized impact on European prices.

TTF prices surged sharply following the outbreak of the war, reflecting Europe’s heavy dependence on Russian gas. While prices initially spiked, they briefly pulled back before rallying again as supply concerns deepened and the market repriced longer-term scarcity.

Henry Hub, on the other hand, reacted differently. The initial move was relatively muted, but prices gradually trended higher in the following weeks and months. This was driven by stronger LNG exports, tighter domestic balances, and increasing global demand for U.S. LNG.

Long CME Henry Hub Natural Gas Futures (NGK2022)

Entry: USD 5.50/MMBtu

Exit: USD 7.20/MMBtu

PnL: 10,000 × (7.20 – 5.50) = USD 17,000

Market participants can also utilise CME Micro Henry Hub Natural Gas Futures to implement a similar position. However, the micro contract was only introduced later (launched on 06 November 2023) and was not available during the 2022 period.

Long CME Micro Henry Hub Natural Gas Futures (Illustrative Equivalent)

Entry: USD 5.50/MMBtu

Exit: USD 7.20/MMBtu

PnL: 1,000 × (7.20 – 5.50) = USD 1,700

While the drivers behind the 2022 rally may not fully apply today, the broader dynamic remains similar. Henry Hub may not react sharply to global shocks, but it tends to grind higher over time when LNG demand strengthens and global balances tighten.

This content is sponsored.

MARKET DATA

CME Real-time Market Data helps identify trading setups and more effectively express market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs at tradingview.com/cme.

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed.

This note explores the divergence, key constraints limiting U.S. gas prices, and what the current setup implies for Henry Hub in the months ahead.

GLOBAL SHOCK HITS HARD ABROAD WHILE U.S. GAS STAYS GROUNDED

The Iran war, which began on 28/Feb, triggered a sharp repricing across global energy markets, with natural gas seeing one of the strongest reactions.

Disruptions to the Strait of Hormuz, through which roughly 20% of global LNG flows, significantly tightened global supply. Additionally, attacks on Qatar’s Ras Laffan Industrial City alone have taken out about 17% of LNG capacity, with repairs expected to take three to five years.

As a result, global gas prices surged, particularly in Europe (TTF) and Asia (JKM), as markets priced in both immediate disruptions and longer-term supply losses.

The sharp rise in TTF and JKM prices reflects both immediate supply disruptions and potential multi-year capacity losses.

In contrast, Henry Hub has seen a much more muted response. Prices have moved higher, but only modestly.

This divergence highlights a key structural feature of the gas market: Henry Hub remains largely driven by domestic fundamentals.

The outperformance of the TTF can be attributed to several factors:

- Europe relies heavily on LNG imports and must compete for cargoes in a tight market.

- Storage levels are below average, leaving the region more exposed.

- The loss of Qatari supply has introduced concerns around longer-term scarcity.

- Henry Hub's upside is capped by strong U.S. supply, comfortable storage, and limited LNG export capacity.

The chart below shows EU gas storage levels relative to the 5-year average, currently sitting near the lower end of the range.

Source: Swiss Federal Office of Energy

Overall, while Henry Hub has moved in the same direction, the magnitude has been far smaller, reinforcing that U.S. gas prices remain largely insulated from global dislocations.

DOMESTIC CONSTRAINTS: WHY HENRY HUB CANNOT FULLY REPRICE

Despite tightening global LNG markets, Henry Hub’s upside remains limited by domestic fundamentals.

U.S. supply remains strong, and inventories are still at comfortable levels. At the same time, LNG export capacity is already running at full capacity, leaving little room to increase volumes, even as global prices surge.

Source: EIA Natural Gas Storage Data

While a larger-than-expected withdrawal of 132 Bcf (week ending 27/Feb) reflected strong winter demand, overall storage levels have not come under significant stress since the war began.

Source: EIA and Investing.com

On the supply side, U.S. production remains robust. Output has averaged around 109.6 Bcf/d in March, while 2025 production hit a record 118.5 Bcf/d. Production is expected to grow further in 2026, reinforcing the strength of domestic supply.

According to LSEG data, U.S. LNG exports are currently running at approximately 19 Bcf/d, with export terminals operating near full capacity and little spare capacity available.

This creates a key constraint; despite strong global demand, the U.S. cannot significantly increase exports in the short term. As a result, even though global arbitrage opportunities have widened sharply, at times exceeding 200%, Henry Hub has not seen a comparable price surge.

Looking ahead, supply growth may also face delays. At CERAWeek, the CEO of Freeport LNG noted that geopolitical disruptions could slow new project timelines due to constraints in materials, labour, and supply chains.

KEY DRIVERS IN THE MONTHS AHEAD

Looking ahead, Henry Hub is likely to remain supported but not fully re-rated in line with global benchmarks.

On the bullish side, persistent global LNG supply disruptions, particularly from Qatar, are expected to sustain strong demand for U.S. exports, providing a structural floor to prices

However, prices will be anchored to U.S.-centric factors such as:

- Export capacity constrained at 19 Bcf/d.

- Strong domestic production.

- Weather-driven demand.

Weather forecasts will play a key role in Henry Hub’s price action in the coming months. As winter draws to a close in March, prices often soften amid lower heating demand and rising storage injections, before finding support again in the summer (June -August) due to air-conditioning load.

OPTIONS MARKET SIGNALS LIMITED DOWNSIDE WITH UPSIDE TAIL RISK

Options positioning in Henry Hub shows a bullish setup, with a put-call ratio of 0.67.

Source: CME QuikStrike

However, the structure of positioning is more telling. There is meaningful open interest in far out-of-the-money calls (above USD 4), indicating the market is pricing upside tail risk, a scenario where prices could spike if supply disruptions worsen.

At the same time, put positioning is concentrated close to current levels, suggesting that the market sees limited downside from here.

Source: CME QuikStrike

In short, the options market is not aggressively bullish, but it is clearly skewed toward asymmetric upside risk, with downside seen as relatively contained.

HISTORICAL EXAMPLE

The Russia-Ukraine War created a similar backdrop, where disruptions to global gas flows had an immediate and outsized impact on European prices.

TTF prices surged sharply following the outbreak of the war, reflecting Europe’s heavy dependence on Russian gas. While prices initially spiked, they briefly pulled back before rallying again as supply concerns deepened and the market repriced longer-term scarcity.

Henry Hub, on the other hand, reacted differently. The initial move was relatively muted, but prices gradually trended higher in the following weeks and months. This was driven by stronger LNG exports, tighter domestic balances, and increasing global demand for U.S. LNG.

Long CME Henry Hub Natural Gas Futures (NGK2022)

Entry: USD 5.50/MMBtu

Exit: USD 7.20/MMBtu

PnL: 10,000 × (7.20 – 5.50) = USD 17,000

Market participants can also utilise CME Micro Henry Hub Natural Gas Futures to implement a similar position. However, the micro contract was only introduced later (launched on 06 November 2023) and was not available during the 2022 period.

Long CME Micro Henry Hub Natural Gas Futures (Illustrative Equivalent)

Entry: USD 5.50/MMBtu

Exit: USD 7.20/MMBtu

PnL: 1,000 × (7.20 – 5.50) = USD 1,700

While the drivers behind the 2022 rally may not fully apply today, the broader dynamic remains similar. Henry Hub may not react sharply to global shocks, but it tends to grind higher over time when LNG demand strengthens and global balances tighten.

This content is sponsored.

MARKET DATA

CME Real-time Market Data helps identify trading setups and more effectively express market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs at tradingview.com/cme.

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed.

Full Disclaimer - linktr.ee/mintfinance

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Full Disclaimer - linktr.ee/mintfinance

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.