After recent geopolitical noise and US employment data, this second week of January marks the major return of US inflation indicators through the CPI and PPI releases. While the sharp drop in inflation in November surprised markets, real-time inflation measures now appear to have fallen back below 2%. Is this credible? Has US inflation truly been defeated, allowing the Federal Reserve to resume cuts to the federal funds rate in the first quarter of 2026?

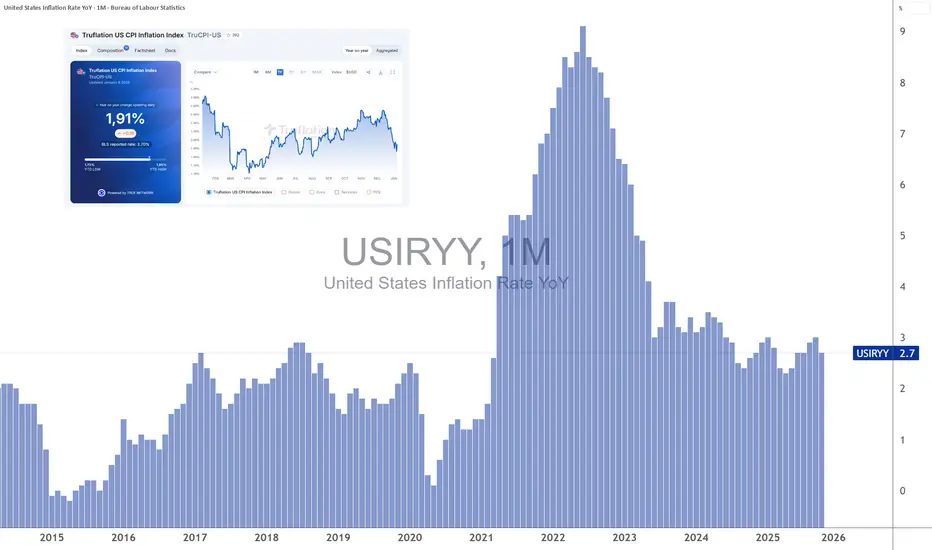

Tuesday, January 13, 2026, brings the release of US inflation data via the CPI index. Recall that the previous update showed headline US inflation declining to 2.7%, with core inflation easing to 2.6%. This decline surprised the market, and the key issue surrounding the January 13 release is whether it confirms the renewed disinflationary trend in the US economy.

It is worth noting that several highly respected real-time inflation indicators, particularly the CPI and PCE estimates provided by Truflation, have already returned to the Federal Reserve’s 2% target, or even slightly below it.

Truflation’s data currently indicate real-time CPI inflation around 1.9%, with PCE inflation slightly above 2%, yet still very close to the Fed’s target. These indicators, updated daily, offer an advanced view of price dynamics well ahead of official statistics, which are published with a delay. Historically, Truflation has often captured inflation turning points more quickly, explaining the growing attention paid to these measures by institutional investors.

Beyond these aggregate indicators, leading components of inflation also confirm a disinflationary environment. ISM PMI indices, for both manufacturing and services, show a renewed decline in their price-related components. This suggests that upstream inflationary pressures along the value chain continue to ease, reducing the risk of an inflation rebound in the coming months.

Real estate, long a key driver of inflation persistence, no longer appears to be a major risk factor. Zillow’s rent index shows rental inflation close to 2%, signaling that normalization is now largely complete. Given the time lag between market rents and their inclusion in the official CPI, this trend supports continued disinflation in the housing component of CPI during the first half of 2026.

Finally, the energy factor clearly supports a disinflationary scenario. Year-over-year oil price changes are now negative, mechanically exerting downward pressure on headline inflation and limiting second-round effects. As long as this dynamic persists, it acts as a powerful buffer against any resurgence in inflation.

In this context, the key question may no longer be whether US inflation will sustainably fall below 2%, but rather how long the Fed will wait before adjusting its monetary policy accordingly. If January CPI and PPI data confirm the trajectory suggested by real-time indicators, market expectations for a resumption of rate cuts as early as the first quarter of 2026 could strengthen rapidly.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

Tuesday, January 13, 2026, brings the release of US inflation data via the CPI index. Recall that the previous update showed headline US inflation declining to 2.7%, with core inflation easing to 2.6%. This decline surprised the market, and the key issue surrounding the January 13 release is whether it confirms the renewed disinflationary trend in the US economy.

It is worth noting that several highly respected real-time inflation indicators, particularly the CPI and PCE estimates provided by Truflation, have already returned to the Federal Reserve’s 2% target, or even slightly below it.

Truflation’s data currently indicate real-time CPI inflation around 1.9%, with PCE inflation slightly above 2%, yet still very close to the Fed’s target. These indicators, updated daily, offer an advanced view of price dynamics well ahead of official statistics, which are published with a delay. Historically, Truflation has often captured inflation turning points more quickly, explaining the growing attention paid to these measures by institutional investors.

Beyond these aggregate indicators, leading components of inflation also confirm a disinflationary environment. ISM PMI indices, for both manufacturing and services, show a renewed decline in their price-related components. This suggests that upstream inflationary pressures along the value chain continue to ease, reducing the risk of an inflation rebound in the coming months.

Real estate, long a key driver of inflation persistence, no longer appears to be a major risk factor. Zillow’s rent index shows rental inflation close to 2%, signaling that normalization is now largely complete. Given the time lag between market rents and their inclusion in the official CPI, this trend supports continued disinflation in the housing component of CPI during the first half of 2026.

Finally, the energy factor clearly supports a disinflationary scenario. Year-over-year oil price changes are now negative, mechanically exerting downward pressure on headline inflation and limiting second-round effects. As long as this dynamic persists, it acts as a powerful buffer against any resurgence in inflation.

In this context, the key question may no longer be whether US inflation will sustainably fall below 2%, but rather how long the Fed will wait before adjusting its monetary policy accordingly. If January CPI and PPI data confirm the trajectory suggested by real-time indicators, market expectations for a resumption of rate cuts as early as the first quarter of 2026 could strengthen rapidly.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

This content is written by Vincent Ganne for Swissquote.

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only and does not constitute investment, legal or tax advice.

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only and does not constitute investment, legal or tax advice.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

This content is written by Vincent Ganne for Swissquote.

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only and does not constitute investment, legal or tax advice.

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only and does not constitute investment, legal or tax advice.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.