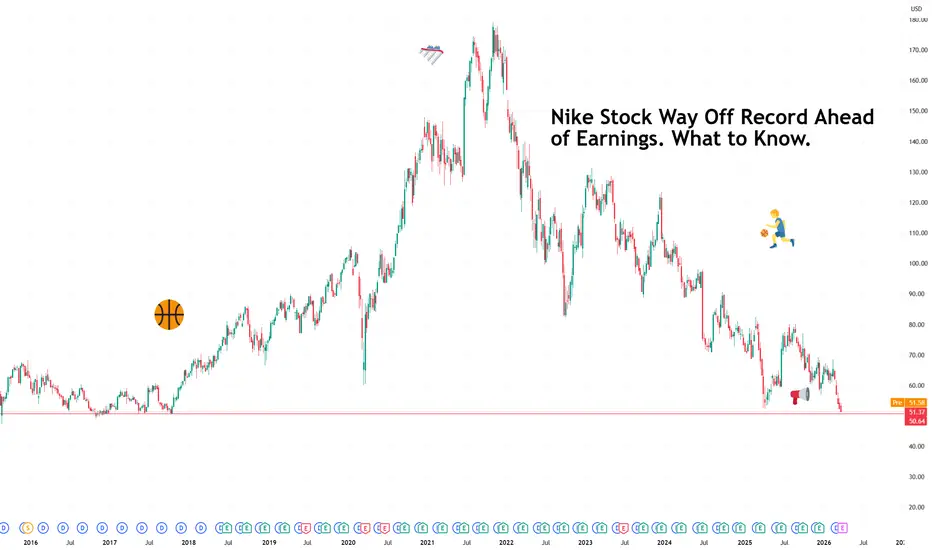

Nike Stock Way Off Record Ahead of Earnings. What to Know.There is a particular kind of corporate humbling that comes not from collapse but from irrelevance creeping in at the edges.

Nike NYSE:NKE is still the world's largest sportswear brand, still moving tens of billions in revenue, still on the feet of more athletes than any other company on earth.

And yet at around $50 a share, nine-year lows, off 70% from its 2021 peak, the stock is asking a question the company has to answer on Tuesday: So how’s that reset going? (insert "well we’re waiting.gif")

The earnings calendar rolls on with Nike’s earnings day next .

📉 How Did We Get Here?

Nike's November 2021 high of $178 looks almost fictional from today's vantage point. The shares are lower by more than 20% this year alone and have spent the past several months hovering near levels last seen when athleisure was still a novelty.

The company is in the middle of what it calls a business reset , refocusing on wholesale partnerships after a years-long push toward selling direct to consumers that did not deliver the margins management had anticipated.

Wholesale means selling through retailers like Foot Locker rather than exclusively through Nike's own stores and app. The retreat is sensible but the execution has been choppy, and the market has been keeping score.

🌍 Three Problems, One Earnings Call

Investors heading into Tuesday's report are watching three specific pressure points.

Europe is slowing. Consumer confidence across the continent has softened, and discretionary spending, the kind that goes on premium trainers, tends to be the first casualty when household budgets tighten.

The US wholesale business, the very channel Nike is trying to reinvigorate, remains unhealthy. Rebuilding retailer relationships after deprioritizing them takes time, and the inventory and shelf-space dynamics are still normalizing. All the while profits are slumping .

Outside the tariff woes from a year ago , China continues to disappoint. The post-pandemic recovery that Nike and many other consumer brands were counting on has been more stubborn than anticipated, with local competitors gaining ground and consumer sentiment remaining soft.

The market is expecting revenue of roughly $11.1 billion for the quarter, flat year on year, an improvement on the 9.3% decline recorded in the same period last year.

Earnings per share, meaning profit divided across all outstanding shares, is expected to land at 29 cents. Last quarter Nike beat on both revenue and earnings, so the bar exists, even if it is not set particularly high.

👟 The Cool Factor Problem

Beyond the financials, Nike has a cultural challenge that balance sheets struggle to capture. The brand that defined athletic aspiration for four decades is working harder than usual to stay relevant.

Its answer, at least partly, is a sneaker called Mind, a shoe focused on mindfulness. Whether a mindfulness sneaker moves the needle on coolness is a question the market will eventually answer, but it is the kind of product that signals a company actively searching for its next identity.

🆕 New Balance Is Having a Moment

While Nike searches, New Balance is sprinting. The 120-year-old brand, once synonymous with sensible footwear for people who prioritize comfort over style, grew sales 19% last year and 180% since 2020.

It has raised average prices by roughly 30% over the past five years, proving consumers will pay a premium for a brand they believe in. It opened 80 new stores last year, aggressively rebuilding physical retail presence at the exact moment Nike was stepping back from it.

New Balance expects to cross $10 billion in sales this year, putting it roughly $2 billion behind Nike's quarterly revenue run rate. That gap is closing, and it is closing fast.

🎯 What to Watch Tuesday

The headline numbers are important, for sure, but the language around China and wholesale recovery will tell the more important story. So grab your two shares and listen for whether management sounds like a team executing a plan or a team revising one.

At $50, Nike is cheap relative to its own history. Cheap and done falling are different things, though.

Off to you : What’s your outlook for Nike? Share your views in the comments!

Nike

SinnSeed | #Nike (#NKE) in 2026 - idea - 26.02.2026🗓 SinnSeed | #Nike (#NKE) in 2026: the tariff window the market hasn’t priced in yet

🕯 As of February 26, 2026, NKE is trading around 64 USD (63.40–65.00), with a market cap of ~94–95 bn USD.

💼 Dividend yield is roughly 2.5% (0.41 USD per share; record date: March 2). At these levels, this is not a story about an “perfect company,” but about skewed expectations and a potentially meaningful re-rating.

📈 Where Nike stands today

Nike is in the middle of a restructuring under CEO Elliott Hill. Management views FY2026 as a transition year: rapid actions to restore sales without permanent discounting, strengthen partner retail channels, refresh the product portfolio, and reduce the share of “aged” inventory. Improvements are starting to show, but the stock price reflects them only partially.

🛒 What looks strong

North America (about 45% of revenue) is recovering noticeably. Partner (wholesale) sales in Q2 grew 8%. Inventory is coming down and the markdown mix looks healthier—an important sign Nike is gradually regaining control over pricing and demand. Product momentum in running, basketball, kids, and Jordan provides additional support.

📉 What continues to weigh

The main weak spot is Greater China: a soft consumer, competition from Anta and Li-Ning, plus consumer nationalism. Nike’s direct digital sales continue to decline (NIKE Digital -14% in Q2). Gross margin in Q2 fell by 300 bps, with a meaningful portion driven by tariffs.

🗺 And importantly: Nike has already baked in about 1.5 bn USD of annual incremental tariff costs in FY2026.

🧮 Regional snapshot (Q2 FY2026, through November 30, 2025)

Total revenue: 12.43 bn USD (+1% YoY reported).

North America: 5.633 bn (+9%).

EMEA (Europe, Middle East & Africa): 3.392 bn (+3% reported).

Greater China: 1.423 bn (-17%).

Asia Pacific & Latin America: 1.667 bn (-4%).

North America and EMEA represent nearly three quarters of the business and remain resilient, while China and other regions continue to drag on the overall picture.

⏱ Core idea for 2026: tariffs may flip from a “headwind” into a “tailwind”

After the US Supreme Court ruled the IEEPA-based tariff framework unlawful, the administration shifted to Section 122 (15%), set to run until July 24, 2026 without Congressional approval. The market reacted emotionally to the headline, but has not fully modeled what may matter more: partial or full removal by the deadline and possible refunds of previously paid duties. Wharton estimates the industry is discussing up to 175 bn USD in potential refunds; for Nike, that could mean the already-modeled 1.5 bn USD cost headwind turns into a one-off cash inflow and a margin boost.

⚖️ The price action supports the underpricing thesis: a short-term pop on the news followed by a pullback—classic “sell the fact,” without a deep scenario repricing.

🎯 NKE price scenarios by end-2026 (from ~64 USD)

🛫 Base case: 75–78 USD (+17–22%). Restructuring stays on track; tariff pressure eases partially. Probability ~55%.

🛫 Bull case: 85–92 USD (+33–44%). Section 122 is removed/neutralized by July and duty refunds reach 50–70% of the modeled 1.5 bn USD. Probability ~35%.

🛫 Bear case: 55–60 USD (-6–14%). Shift to harsher tariff mechanisms plus further deterioration in China. Probability ~10%.

✍️ My midpoint target: 82–85 USD by December 2026 (+28–33%).

💵 Why Nike could outperform peers

Because Nike’s tariff factor is among the largest in absolute dollars, import dependence is high, and margin expectations are already depressed. If the tariff window starts to close, the impact on earnings and valuation could be disproportionately strong.

🗓 Watchlist calendar

Over the next 2–4 weeks: track news on duty refunds and importer lawsuits.

March 19: Q3 earnings (key question: does North America strength persist?).

April–July: peak catalyst window ahead of the July 24 deadline.

⚠️ Key risks

A shift to a tougher tariff framework, no guarantee of full refunds due to legal complexity, and prolonged weakness in China slowing margin recovery.

💡 Bottom line

Nike in 2026 is one of the more interesting retail setups precisely because of the tariff window. The market is still reacting cautiously—and that can be the opportunity. Building a position on pullbacks below 62 USD makes sense, and a move above 80 USD looks achievable if the tariff narrative turns more favorable into July.

NFA | DYOR

With respect to everyone,

Yours, 🫡 #SinnSeed

45% minimum by May?Nike has delivered strong earnings, even with the imposition of tariffs, but what could be the catalyst for a rally that allows it to recover value over the next four months? Perhaps the new acquired economies generated by Trump’s actions, I am referring to Venezuela. These artificial expansions of the economy could help drive an expansion in corporate multiples.

$NKE: The "Repair Job" in Progress for NIKE👟👟

Nike is currently like a classic sneaker getting dusted down and cleaned up.

It’s not quite "dead money," but it’s definitely not back to full speed yet.

The "Hype" (Why Bulls like it)

The Big Bosses are Buying: CEO Elliott Hill and even Tim Cook (Apple CEO/Nike Board) just dropped millions of their own cash into NYSE:NKE shares. Usually, when the insiders buy the dip, they know something we don't.

Back to Basics: Nike is ditching the "lifestyle" fluff and winning again in Performance Running (up 20% recently!).

North American sales are finally waking up, proving the "Win Now" strategy isn't just a slide deck.

The "Haters" (Why Bears are wary)

China is Still "Meh": Sales in China have been sliding for over a year. It's a tough market to crack right now.

Tariff Trouble: Global trade drama and higher costs are eating into the profits (margins are down about 3%).

The Wait: Management says it’s "middle innings" of a comeback. In other words: bring your patience.

The Bottom Line

If you believe in the "Insider Effect" and the running shoes reboot, this is your entry zone. If you need proof, wait for the $69 breakout.

#NKE #Nike #Turnaround #ValuePlay #TechnicalAnalysis

Trend is your Friend. #NKE is a prime example...fade the bullish moves

look for continuation down

that is going to be the money maker

shorting into resistance

not longing on reversals

Is Nike Long A Good Play ? - AnalysisWhy Nike’s Stock Has Fallen So Far

Nike’s share price has declined significantly for several interrelated reasons:

1. Slowing Revenue & Profit Growth

Nike’s revenue growth has been slowing, with some periods of low single-digit (+1%) year-over-year sales growth and even expected declines in certain quarters that disappointed markets.

2. Margin Pressure

Gross margins have compressed due to higher tariffs, discounting to clear excess inventory and rising costs, a headwind that has dragged down profitability.

3. Weakness in China

Nike’s sales in Greater China have repeatedly declined, with some quarterly drops exceeding 15%, hurting growth expectations in a once-high-potential market.

4. Strategic & Operational Challenges

Nike’s pivot toward direct-to-consumer (DTC) sales and online has been uneven, early gains have stalled, forcing mix adjustments and inventory clean-ups that weighed on financials.

5. Competitive Pressure

Smaller, trendier brands (like On and Hoka) have eroded Nike’s premium market share in key categories, and fierce competition has pressured both pricing and brand perception.

6. Debt & Credit Ratings

Nike’s credit rating was downgraded somewhat due to profit and revenue headwinds, reflecting increased cost pressures and expectations of tighter cash flow, though the company remains investment-grade.

7. Market Sentiment & Volatility

Even when Nike posted better-than-expected earnings, the stock often dropped as investors focused on margins and outlook rather than current results.

Key Financial Metrics (Fundamentals Snapshot)

From the most recent fundamental data available:

-Revenue (TTM): ~ $46.5 billion

-Net Profit (TTM): ~$2.5 billion

-Gross Margin: ~ 41%

-Net Profit Margin: ~ 5.4%

-Debt/Equity: ~ 57%

(TTM = trailing 12 months)

This shows Nike still generates profit and sizable sales, but margins have narrowed compared to historical performance.

Bullish Case :

Strong Brand, Global Market Leader

Nike is one of the most recognized apparel/footwear brands globally with decades of brand equity, wide distribution, and premium pricing power in many segments.

Dividend Yield & Buybacks

Lower share price has lifted Nike’s dividend yield to around 2.5%, providing income appeal, and the company has a long history of returning capital to shareholders through dividends and buybacks.

Contrarian Value Appeal

At significantly lower multiples than in previous years, some analysts (e.g., at Barron’s) argue the stock is undervalued relative to sales (e.g., 2.1× sales near historic lows), and there’s potential upside if turnaround strategies gain traction.

Turnaround Initiatives Underway

New leadership is refocusing strategy, correcting promotional excesses, restoring wholesale relationships, refining product mix and improving inventory posture, which may pay off over time.

Bearish Case :

Revenue & Profit Challenges

Nike’s revenue growth has been uneven, with some quarters showing near-flat or declining top line, and margins are under pressure from discounts, tariffs and inventory cleanup.

China & Global Weakness

Persistent weakness in the Chinese market, which once was a growth engine, continues to drag on results.

Competition & Brand Challenges

Younger, trendier brands have captured some share, especially in running and lifestyle categories, pressuring Nike’s traditional dominance.

Cash Flow & Dividend Sustainability

Some analysts express concern over cash flow supporting current capital returns if earnings continue to weaken.

Debt Considerations

Though still investment-grade, Nike’s credit downgrade signals caution about leverage and profitability in the near term.

Consumer Discretionary Risk

As a consumer discretionary stock, Nike is sensitive to economic cycles, downturns in consumer spending could further pressure sales.

Disclaimer:

This analysis is for informational and educational purposes only and does not constitute financial advice, investment recommendation, or an offer to buy or sell any securities. Asset prices, valuations, and performance metrics are subject to change and may be outdated. Always conduct your own due diligence and consult with a licensed financial advisor before making investment decisions. The information presented may contain inaccuracies and should not be solely relied upon for financial decisions. I am not a licensed financial advisor or professional trader. I am not personally liable for your own losses; this is not financial advice.

fundamental NIKE analysis suggest long term upAfter massive price decrease NIKE is at a good level to buy into. Fundamentals are ok while the price dropped significantly. Showing negative correlation between low price and ok fundamentals.

NKE NIKE Options Ahead of EarningsIf you haven`t sold NKE before the previous earnings:

Now analyzing the options chain and the chart patterns of NKE NIKE prior to the earnings report this week,

I would consider purchasing the 69usd strike price Calls with

an expiration date of 2025-12-19,

for a premium of approximately $2.51.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

NIKE SHORT TRADING PLANI am shorting Nike because its long-term trend is downward, and the lower line represents a support level. I’m also basing my short position on RSI signals.

Nike by April 2025 we should have break out or breakdown !101 Trend lines analysis. By April we should could/might reach the Red line in which we will have a break out to a new ATH in the next years or so or a break down to the 40ish/50ish region.!

Nike's 1984 Vs 2000 Major Trend lines The 1984 Major and historical Trend line is already broken with 3 candles below, technially

this is a valid and confirmed breakdown.

The 2000 Major and historical Trend line is hanging by $5 give or take $66 -+ is the support for the TL.

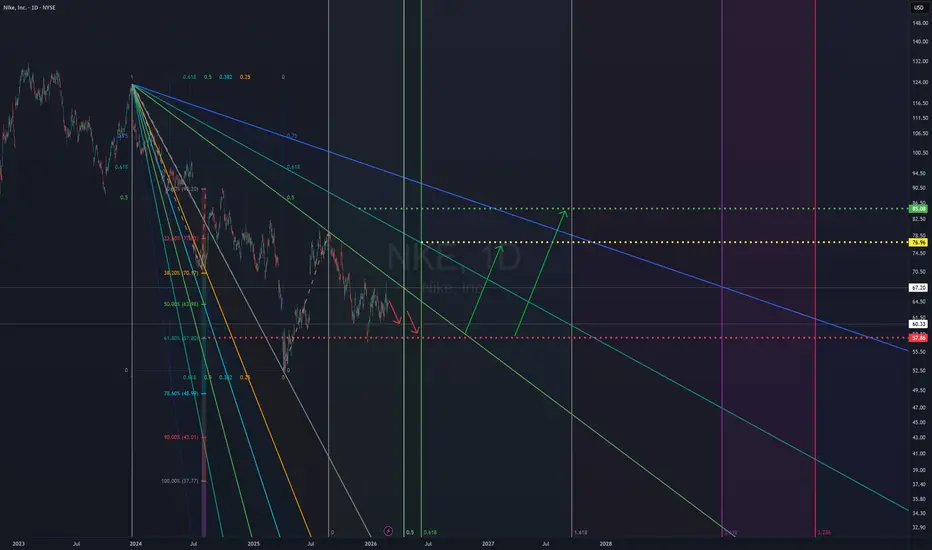

NIKE — $31–$11 bottom | Before SuperCycle Wave 3 hits ~$1000⚡ NKE: Micro Wave 4 Bounce Before the Final Flush 👟🔥

Nike ( NYSE:NKE ) has been in a SuperCycle Wave (2) correction since topping near $179 in 2021. This isn’t a collapse — it’s a structured reset that should run into 2027 , forming a large ABC correction before the next SuperCycle Wave (3) bull phase begins.

Right now, price action is inside a micro Wave 4 move within the ongoing Wave A. Micro waves 1, 2, and 3 have completed, and waves A and B of this current wave 4 are also done. What’s likely next is a short-term bounce toward $82 , where equal highs and liquidity sit, before a final Wave 5 decline finishes Wave A around the 0.236 Fibonacci retracement near $31 .

From there, expect a Wave B rebound followed by Wave C down toward the 0.382 retracement around $11 , which could complete the full SuperCycle Wave (2) correction. That zone may become the macro accumulation area ahead of the next explosive SuperCycle rally.

The $82 region aligns with a liquidity grab in Smart Money terms — a trap for breakout buyers before price descends into the deeper $31–$50 institutional value range , matching demand zones from 2016–2018.

This phase is less about panic and more about patience. Once the 2021–2027 correction ends, Nike could begin a multi-year rally that redefines its valuation.

The swoosh isn’t breaking — it’s recharging for its next leap. 👟⚡

#NKE #Nike #ElliottWave #SmartMoneyConcepts #WaveTheory #Fibonacci #PriceAction #MarketCycle #TechnicalAnalysis #TradingViewAnalysis #StocksToWatch

Global Brand Power Driving Growth Opportunity: BUYBuy Reason: Nike’s strong brand presence, global market penetration, and innovation in sportswear position it for steady revenue growth and resilience amid market fluctuations. Its expanding digital sales and product innovation make it attractive for long-term investors.

UPS BACK TO 120 BY 2026 See new posts

WRITE A SMALL POST ABOUT TRADING MAG 7 STOCKS ON NYSE

Trading the "Magnificent 7" stocks—Apple, Microsoft, Nvidia, Amazon, Meta, Alphabet, and Tesla—on the NYSE offers high potential but comes with unique challenges. These tech giants drive market trends, boasting massive market caps and innovation-driven growth. Their volatility, fueled by earnings reports, product launches, and macroeconomic shifts, creates opportunities for traders. Focus on technical analysis (RSI, moving averages) and stay updated on news like regulatory changes or AI advancements impacting their sectors. Diversify within the group to hedge risks, and use stop-loss orders to manage volatility. Trade smart, stay informed! #Mag7 #NYSE #StockTrading

WRITE A SMALL POST ABOUT WHY ADOBE CAN REACH WITH SOME TECHNICAL REASONS 510 BY 2026

Browsed tradingview.com

Show All (4)

Why Adobe (ADBE) Could Hit $510 by 2026: Technical Breakdown Adobe's trading at ~$365 today, but bullish setups scream upside. Here's why $510 (40% gain) is in play:Bullish Triangle Breakout: ADBE's consolidated in a multi-year ascending triangle since 2020. A recent close above $370 resistance (near 50-day MA ~$383) signals breakout, targeting $510 (measured move from base at $330 low).

RSI Rebound: At 42 (neutral, not oversold), RSI is coiling for momentum shift. Weekly RSI >50 could trigger buy signals, aligning with AI-driven catalysts like Firefly integrations.

MACD Crossover Potential: MACD histogram narrowing (-5.26) hints at bullish crossover by Q4 2025. Paired with 200-day MA (~$420) as next support, this flips sentiment to "Strong Buy" per TradingView.

Analyst Backing: Consensus targets $465–$496 short-term, but long-term forecasts (e.g., LongForecast) eye $577 EOY 2026 on 11% revenue growth to $23B+.

Volatility ahead, but AI tailwinds make this a no-brainer long. What's your PT? #ADBE #StockTrading #TechnicalAnalysis

WITE SOME GOOD REASONS WHY TESLA CAN REACH 450 THEN 500 BY EOY OR 2026

Searched for "reasons Tesla stock to reach $450 $500 by end of 2026"

10 results

Show All (3)

Why Tesla (TSLA) Could Hit $450 Then $500 by EOY 2025 or 2026: Key Catalysts Tesla's hovering around $315 today (as of Sept 23, 2025), down ~20% YTD amid sales dips, but the setup for a rebound to $450 (43% upside) and $500 (59% upside) is primed by execution on autonomy, EVs, and energy. Here's the bull case, blending fundamentals and forecasts:Robotaxi & FSD Rollout Momentum: Tesla's Cybercab unveil in Oct 2025 could catalyze a surge, with unsupervised Full Self-Driving (FSD) v13 hitting highways by year-end. ARK Invest's base case eyes $4,600 by 2026 (driven 60%+ by autonomy), but even conservative models like CoinCodex forecast $453 avg in 2026, with highs to $664 on ride-hailing revenue potentially adding $10T market value.

2 sources

Piper Sandler just hiked their PT, calling TSLA the "top idea" for AV investing.

EV Delivery Rebound & Affordable Models: Post-2025 sales weakness (1.8M deliveries est.), expect 2.3M+ in 2026 with Model 2 launch (~$25K EV) ramping production to 3M+ annually. This counters China/EU headwinds, recaptures 20%+ US market share, and boosts EPS to $0.49 next quarter—fueling a $450 breakout per LongForecast's Q3 2026 path.

2 sources

Morningstar sees a 2026 revival echoing 2016's Model 3 surge.

Energy Storage Boom: Megapack deployments exploding (Q2 2025: 9.4 GWh), with 50%+ YoY growth projected through 2026, diversifying revenue to 15%+ of total. This hedges EV volatility, pushing margins to 20%+ and supporting $500 on 11% revenue growth to $130B.

Optimus Humanoid Robot Sales: External sales kick off late 2025/early 2026, targeting $20K/unit with factory pilots scaling to millions. This could add $1T+ valuation long-term, per ARK, but even modest adoption lifts sentiment to $500 by EOY 2026.

2 sources

Analyst consensus (51 firms) averages $391 short-term, but bulls like Fubon ($1,000) and CoinPriceForecast ($526 EOY 2026) back the push.

2 sources

Risks like Musk drama or tariffs loom, but flawless execution flips this to moonshot territory. Long TSLA? #TSLA #EVRevolution #StockForecast

10 web pages

WRITE A OST ABOUT RDW STOCK REACHING 13 DOLLARS BY 2026

Searched for "RDW stock OR Redwire forecast OR price target since:2025-01-01"

9 results

Show All (3)

Why Redwire (RDW) Could Blast to $13 by 2026: Bull Case RDW's trading at ~$9 today (Sep 23, 2025), down post-Q2 earnings miss, but with space infrastructure booming, $13 (44% upside) is conservative amid analyst love and catalysts. Here's the setup:Analyst Consensus Screams Upside: 8 firms rate "Buy" with avg PT $16.56–$18.64 (83–107% gain short-term), max $28—easily clearing $13 by EOY 2026 on execution. Even bears like BofA's $10 see room for rebound; H.C. Wainwright holds $22 Buy post-acquisition.

4 sources

Zacks ABR 1.00 (Strong Buy) backs $26 avg.

NASA & Defense Contract Pipeline: $25M NASA IDIQ award (Aug '25) for space tech, plus prime for Skimsat and Honeywell quantum collab—fuels 20%+ YoY revenue to $550M+ in 2026. Artemis funding stability hedges risks, per Roth MKM Buy.

Edge Autonomy UAS integration adds drone revenue, targeting $100M backlog growth.

Acquisition Synergies & Margin Expansion: Q2's Transformative Acquisition (e.g., Hammerhead integration) boosts EPS from -$1.41 to break-even by Q4 '25, with 132M Q3 revenue est. up 15%. Analysts eye 25% margins by 2026 on in-space manufacturing scale.

2 sources

Space Economy Tailwinds: $1T market by 2040; RDW's solar arrays, 3D printing IP position it for 30% sector growth. CoinCodex forecasts $8.41 avg '26 low-end, but bulls like Canaccord ($17.50) see $13 as floor on 11% EPS ramp.

2 sources

Volatility from govt reliance, but flawless delivery flips this to orbit. Long RDW? #RDW #SpaceStocks #StockForecast

7 web pages

WRITE A SMALL POST ABOUT AMD REACHING 200 THEN 240 LONG TERM BY 2026

Searched for "AMD analyst price targets 2025 2026"

10 results

Show All (3)

Why AMD (AMD) Could Surge to $200 Then $240 Long-Term by 2026: AI-Powered Bull Case AMD's trading at ~$160 today (Sep 23, 2025), up 30% YTD on AI tailwinds, but with EPS exploding to $6+ in 2026, $200 (25% upside) then $240 (50% gain) is locked in for patient bulls. Here's the roadmap:AI Datacenter Dominance: MI355X GPUs ramping Q4 '25, capturing 20%+ market share from Nvidia via cost-efficient accelerators (40% better tokens/$). Oracle's Zettascale cluster + Meta/Microsoft deals project $40B+ revenue in '26 (21% YoY), per analysts—fueling $200 breakout as datacenter hits 50% of sales.

2 sources

EPS Acceleration & Valuation Pop: Consensus EPS jumps 54% to $6.01 in 2026 (from $3.90 '25), trading at 27x forward P/E—undervalued vs. peers at 0.49 PEG. At 33x (Nasdaq-100 avg), that's $199 EOY '26; bulls like Truist eye $213 short-term, scaling to $242 on 35% growth.

3 sources

Gaming/Quantum Rebound: Ryzen AI CPUs + IBM quantum collab revive gaming (15% YoY) and edge AI, adding $10B+ revenue. MI400 launch '26 cements leadership, per CoinPriceForecast's $242 avg.

2 sources

Analyst Consensus Backs It: 34 firms avg $188 PT (high $230), with LongForecast hitting $296 mid-'26 on momentum. Export risks loom, but flawless execution = moon.

2 sources

Long AMD for the AI decade? #AMD #AIStocks #StockForecast

6 web pages

DO THE SAME WITH CHIPOTLE 50 DOLLARS

Why Chipotle (CMG) Could Climb to $50 by 2026: Tasty Bull Case Chipotle’s trading at ~$43 today (Sep 23, 2025), down slightly YTD, but with strong fundamentals and operational wins, $50 (16% upside) by EOY 2026 is achievable long-term. Here’s the recipe:Revenue & Same-Store Growth: Q2 '25 comps +11.1% and $3.8B revenue (15% YoY) signal robust demand. Analysts project 13% YoY growth to $12.5B in '26, driven by 300+ new stores and digital orders (30%+ of sales). This supports $1.75 EPS, pushing P/E to 28x for a $50 target.

Operational Efficiency: Chipotlanes (drive-thru) now in 60% of new locations, boosting margins to 28%+. Automation in prep (e.g., Autocado) cuts costs 5%, per management, fueling EPS growth to $2.10 by '26, aligning with $50 at 24x forward P/E.

Analyst Optimism: 27 firms avg $50.24 PT (high $62), with BMO Capital’s $56 Buy rating citing loyalty program strength (35M+ members). CoinPriceForecast sees $53 mid-'26, clearing $50 on 10% comps.

Consumer Resilience: Despite inflation, CMG’s premium positioning (health-focused, customizable menu) retains Gen Z/Millennial traffic, hedging macro risks. LongForecast eyes $54 by Q3 '26.

Price wars or labor costs could bite, but Chipotle’s growth engine is sizzling. Long CMG? #Chipotle #StockForecast #FastCasual

WRITE A POST ABOUT LUNAR STOCK INUTIVE MACHINES BACK TO 20 DOLLARS BY 2026

Searched for "LUNR stock forecast 2026 revenue growth"

10 results

Show All (3)

Why Intuitive Machines (LUNR) Could Rocket Back to $20 by 2026: Lunar Bull Case LUNR's trading at ~$9.71 today (Sep 23, 2025), down from its $24.95 peak amid mission hiccups, but with NASA contracts stacking and revenue exploding, $20 (106% upside) is in orbit by EOY 2026. Here's the launch sequence:NASA Contract Avalanche: Fresh $2.5M NextSTEP award (Jan '25) for lunar logistics, plus $4.82B Near Space Network (NSN) for comms/nav through 2029 (extendable to 2034). IM-3 mission in '26 delivers South Pole payloads ($116.9M CLPS), scaling DTE services to $200M+ annually.

5 sources

LTV award mid-'25 adds mobility revenue, hedging risks.

Revenue Hypergrowth: From $217M in '25 to $700M+ in '26 (222% YoY) on dual missions, relay sats, and NSN backlog. EPS flips to $0.03 avg (from -$0.22), trading at 20x forward P/E—undervalued vs. space peers at 30x.

2 sources

Analyst Moonshot Targets: Consensus $15.44 short-term (6 firms, Moderate Buy), but bulls like Canaccord ($26, up from $17.50) and Intellectia ($24.94 Dec '26) eye $20+ on Artemis tailwinds. Highs to $31.88 clear it easy.

5 sources

Artemis & Market Boom: $1T space economy by 2040; LUNR's Nova-C landers + Khon sats position it for 20-30% YoY growth, per Reddit bulls modeling $500M+ revenue at 20x P/S = $100 PT (conservative slice: $20).

Mission delays or funding cuts loom, but flawless IM-3 execution = liftoff. Long LUNR to the Moon? #LUNR #SpaceStocks #LunarEconomy

13 web pages

DO THE SAME WITH UPS

Searched for "UPS stock catalysts 2025 2026"

10 results

Show All (4)

Why UPS (UPS) Could Surge to $100 Then $120 Long-Term by 2026: Logistics Rebound UPS's trading at ~$84 today (Sep 23, 2025), down ~35% YTD on volume softness and Amazon shifts, but with cost cuts unlocking $3B+ savings and e-commerce/reshoring tailwinds, $100 (19% upside) then $120 (43% gain) by EOY 2026 is realistic. Here's the bull thesis:Efficiency Overhaul & Amazon Pivot: Cutting Amazon volumes >50% by mid-2026 frees capacity for higher-margin SMB/premium parcels, boosting domestic margins to 12%+. Network of the Future automation (164 closures, 20K job cuts) delivers $3.5B annual savings by '26, per management—driving $100 on EPS ramp to $7.38 (13% YoY).

3 sources

Revenue & Margin Expansion: Guidance eyes $108-114B revenue in '26 (above $102B est.), with 1% YoY growth accelerating to 4% in '27 on healthcare logistics (Andlauer acquisition) and nearshoring demand in LatAm/Europe. Operating margins hit 13%+, undervalued at 14x forward P/E vs. 5-yr avg 16.5x—pushing to $120 per Goldman Sachs catalysts.

4 sources

EPS Acceleration: Consensus $7.38 EPS in '26 (up 13% from $6.51 '25), with highs to $8.00 on freight recovery and digital investments. At 16x (historical norm), that's $118+; CoinPriceForecast aligns at $114 EOY '26.

2 sources

Analyst Consensus Fuels It: 29 firms avg $104 PT (24% upside, high $145), with "Buy" ratings from Goldman/Raymond James citing mid-'26 profitability inflection. Zacks sees 26% to $112

Nike 1W - Just buy it?Nike is showing signs of a reversal after a prolonged downtrend, holding the key buy zone at 69.52, which aligns with the 0.618 Fibo retracement. The breakout of the descending channel adds weight to a structural shift, with the first target seen around 97.63, where the 1.618 Fibo extension and a major resistance zone converge. A successful breakout above this level would open the path toward 125.73, coinciding with the MA200 and a significant volume cluster. While the MA50 still hovers under price, suggesting caution in the short term, the overall structure points toward a bullish scenario.

Fundamentally , Nike remains solid, supported by recovering consumer demand and cost optimization, while its strong brand and institutional interest create a backdrop for sustained growth.

The tactical outlook favors a bullish continuation as long as price holds above the 69.5 zone, with upside targets at 97.6 and 125.7.

If buyers manage to maintain momentum, the market might just rewrite Nike’s slogan: “Just buy it.”

BUY NOW $LULU EASY MONEYRSI (14) 39.15

P/E 13.65 as of 08/13/2025

Buy now and you will thank me later.

This is super sale

Nike - A buy after pullbackNike's daily chart shows a competed five-wave advance off the lows from 52.28, with a subsequent correction underway. We believe that we are in wave C of this correction which could take prices back to 68-66 levels before another move higher unfolds towards 100.00

NIKE Confirms A Bullish Reversal With An Impulsive RecoveryWe talked about Nike on July 10 with our members, where we mentioned and highlighted a completed higher degree ABC correction in wave IV on the monthly and weekly charts.

Today we want to represent a closer view, as we see a five-wave impulsive recovery away from the lows on a daily chart. It actually confirms the bottom and bullish reversal, but since it can be trading in 5th wave that can stop around 80-85 area, we should be aware of a three-wave corrective setback soon. It can slow down the price back to the open GAP, so ideal buy zone is in the 70-60 area. Invalidation level is at 52.

Highlights:

Direction: Up, but watch out for a correction

Structure: Impulse, Wave 5 in final stages

Support: 70 / 60

Nike - This is the bottom!💉Nike ( NYSE:NKE ) creates the bottom now:

🔎Analysis summary:

More than four years ago, Nike created its previous all time high. We have been witnessing a downtrend ever since and a correction of about -70%. But with the recent retest of an important horizontal structure and bullish confirmation, Nike is about to create a potential bottom.

📝Levels to watch:

$65, $80

🙏🏻#LONGTERMVISION

Philip - Swing Trader

Nike Looks Ready — A Smart Time to Consider InvestingOn the monthly chart, NIKE has been in a downtrend since November 2021, but the signs are pointing toward a potential trend reversal. Here's why I believe the bottom may already be in:

✅ MACD Histogram shows a strong positive divergence, signaling weakening bearish momentum.

✅ The RSI downtrend line has been broken and successfully retested, confirming bullish strength.

✅ A clear hammer candle has formed at a historical wide support zone, showing strong demand.

Now, price is facing three consecutive resistance levels — and with each breakout, the next zone becomes the new target, (87.5 → 102 → 122).

The structure suggests a step-by-step move higher if momentum holds. Keep an eye on the breakout above the descending trendline — that’s where things could accelerate.

NKE NIKE Options Ahead of EarningsIf you haven`t sold NKE before the previous earnings:

Now analyzing the options chain and the chart patterns of NKE NIKE prior to the earnings report this week,

I would consider purchasing the 62usd strike price Calls with

an expiration date of 2025-7-3,

for a premium of approximately $2.29.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

If Nike Were Born Today: The Hypothetical Valuation of a New-AgeAbstract

Nike is one of the most recognizable brands on the planet, yet its valuation often lags behind newer, tech-driven companies with far less global influence. What if Nike were launched today — with its current revenue, market dominance, and brand power — but operated like a modern D2C startup with a tech DNA? This research explores what Nike would be worth in today’s market conditions, showing just how undervalued it may actually be when compared to new-age companies.

1. Introduction

Nike, Inc. (NYSE: NKE) is a global sportswear powerhouse with over $51 billion in annual revenue and a footprint in more than 170 countries. It has shaped athlete endorsement culture, built a generational brand, and transformed consumer behavior. Yet its current market capitalization sits around $80 billion — modest compared to newer players with less revenue but tech-first narratives.

This article dives into a simple but powerful hypothetical:

If a new company replicated Nike's current revenue and global dominance today, how would the market value it?

2. Nike Today: A Snapshot

Metric Value

FY2023 Revenue $51.2 Billion

Market Cap (Apr 17, 2025) ~$80 Billion

Net Profit Margin ~10.5%

P/E Ratio (TTM) ~17.9

Brand Value (Forbes, 2020) ~$39.1 Billion*

Global Reach 170+ Countries

*According to Forbes' Most Valuable Brands, Nike ranked #13 globally with a brand value of $39.1 billion in 2020. Other rankings (e.g., Interbrand 2023) place Nike's brand value even higher at $53.7 billion.

Despite being a category leader, Nike trades at a modest 1.6x sales multiple, compared to modern companies that command 5x, 7x, or even 30x+ valuations.

3. New-Age Valuation Framework

Today’s market rewards:

Tech-first operations

High-margin D2C models

Recurring revenue (subscriptions, memberships)

Community-driven brand growth

AI, personalization, and digital experiences

Let’s compare valuation multiples:

Company Sector Revenue Market Cap P/S Ratio

Nike Apparel $51.2B $80B ~1.6x

Lululemon Apparel SEED_TVCODER77_ETHBTCDATA:9B $50B ~5.5x

Salesforce SaaS $34B $240B ~7x

Nvidia AI/Chips $60B $2.3T ~38x

4. What Would a “Modern Nike” Be Worth Today?

If a new company today built:

$50B+ revenue

Global presence and branding like Nike

D2C-first, tech-enabled business

40–50% gross margins with scalable digital ops

Then, even at a conservative 6x revenue multiple, its valuation would be:

$50B × 6 = $300 Billion

And that's before factoring in:

AI-driven retail personalization

Creator monetization ecosystems

Loyalty programs and recurring revenue streams

Lower inventory risk with tech-driven fulfillment

5. Brand Value Through Royalty Method

Using the Royalty Relief Method:

Brand-attributable revenue (90% of $51.2B) = FWB:46B

Royalty rate = 6%

Annual royalty = $2.76B

Present Value (8% discount rate):

$2.76B ÷ 0.08 = \boxed{~$34.5B}

Nike’s brand, purely from an intellectual property lens, is worth significantly more than market pricing implies.

6. Why Nike Seems Undervalued

Categorized as a traditional apparel retailer vs. tech-first brand

Slower YoY growth relative to newer disruptors

Wholesale-heavy model impacts margins

Market overlooks its cultural dominance and brand loyalty

If Nike shifted its model to fully digital, leaned into AI and subscriptions, and emphasized platform economics, its valuation could more than double.

7. Conclusion

Nike, if built today, would not be an $80B company — it would likely be valued between $300B and $400B.

That’s the gap investors often miss.

Nike isn’t just a shoe and apparel brand — it’s global IP, media, culture, and influence. Yet in today’s market, it trades like a legacy retailer. If a startup were to achieve what Nike already has, it would be considered a generational tech unicorn.

Nike isn’t overvalued — it’s misunderstood.

About This Research

This research article was developed using AI-powered analytical tools, historical data modeling, and comparative valuation logic to explore hypothetical scenarios around Nike’s valuation. It combines financial fundamentals with modern market heuristics to offer a data-driven perspective on brand valuation in the context of today’s tech-driven economy.

Disclaimer

The information provided in this article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis, opinions, and projections expressed are solely those of the author and are based on publicly available data as of the time of writing. This article is a hypothetical research exploration and should not be interpreted as a recommendation to buy, sell, or hold any securities mentioned herein.

All trademarks, brand names, and company references (including Nike Inc., Nvidia, Salesforce, etc.) are the property of their respective owners and are used for illustrative purposes only. The author is not affiliated with, endorsed by, or sponsored by any of the mentioned companies.

Investing in the stock market involves risk, including the potential loss of principal. Readers are strongly advised to do their own research and consult with a licensed financial advisor or other qualified professionals before making any investment decisions.

Past performance does not guarantee future results. The hypothetical scenarios and valuations discussed in this article are speculative in nature and are not guarantees of future company valuations or performance.

Nike (NKE) Share Price Falls to Lowest Level Since 2017Nike (NKE) Share Price Falls to Lowest Level Since 2017

The chart for Nike (NKE) shows that the share price has dropped to around $55 – levels last seen in November 2017.

Since the start of 2025, the stock has declined by approximately 27%.

Why Has Nike’s Share Price Dropped?

As noted in our analysis from September 2024, Nike shares had been trending downward for several months due to intense competition. However, President Trump’s tariffs have become the dominant bearish factor.

This is largely because Nike relies heavily on manufacturing operations in Asia – many of which have been directly affected by the newly imposed tariffs.

What’s Next?

According to the Wall Street Journal, manufacturers are taking a wait-and-see approach. They’re reluctant to shift production out of Asia, which could mean higher prices for American consumers. A full return to U.S. production is unlikely due to:

→ a shortage of skilled workers and suppliers;

→ significantly higher wages in the U.S. compared to Asia;

→ relocating production from Asia is a complex business migration, not just a factory move – a process many companies might not be prepared for.

Some firms are reducing their margins or optimising logistics, but most are hoping to weather the storm or delay major changes.

Technical Analysis of Nike (NKE) Shares

The price is forming a downward channel (highlighted in red), with the following characteristics:

→ the median line provided temporary support, but the early April rebound attempt was very weak;

→ the lower boundary of the channel now appears to be acting as support.

The RSI indicator suggests strong oversold conditions. Bulls might take comfort in the proximity of the psychological $50 mark strengthening this support level. However, it seems that only positive developments on the tariff front are likely to reverse sentiment meaningfully.

According to WSJ analysts, Trump’s recent comments hint at possible negotiations. But unless the President changes his stance, Mexico, Brazil, and India – nations well-placed to act as intermediaries between China and the U.S. – could emerge as the main beneficiaries.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.