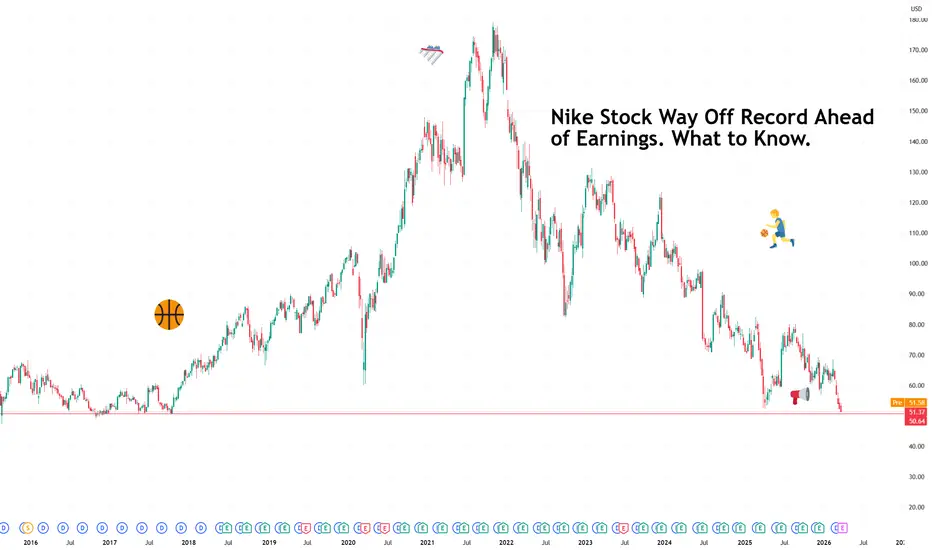

Nike Stock Way Off Record Ahead of Earnings. What to Know.There is a particular kind of corporate humbling that comes not from collapse but from irrelevance creeping in at the edges.

Nike NYSE:NKE is still the world's largest sportswear brand, still moving tens of billions in revenue, still on the feet of more athletes than any other company on earth.

And yet at around $50 a share, nine-year lows, off 70% from its 2021 peak, the stock is asking a question the company has to answer on Tuesday: So how’s that reset going? (insert "well we’re waiting.gif")

The earnings calendar rolls on with Nike’s earnings day next .

📉 How Did We Get Here?

Nike's November 2021 high of $178 looks almost fictional from today's vantage point. The shares are lower by more than 20% this year alone and have spent the past several months hovering near levels last seen when athleisure was still a novelty.

The company is in the middle of what it calls a business reset , refocusing on wholesale partnerships after a years-long push toward selling direct to consumers that did not deliver the margins management had anticipated.

Wholesale means selling through retailers like Foot Locker rather than exclusively through Nike's own stores and app. The retreat is sensible but the execution has been choppy, and the market has been keeping score.

🌍 Three Problems, One Earnings Call

Investors heading into Tuesday's report are watching three specific pressure points.

Europe is slowing. Consumer confidence across the continent has softened, and discretionary spending, the kind that goes on premium trainers, tends to be the first casualty when household budgets tighten.

The US wholesale business, the very channel Nike is trying to reinvigorate, remains unhealthy. Rebuilding retailer relationships after deprioritizing them takes time, and the inventory and shelf-space dynamics are still normalizing. All the while profits are slumping .

Outside the tariff woes from a year ago , China continues to disappoint. The post-pandemic recovery that Nike and many other consumer brands were counting on has been more stubborn than anticipated, with local competitors gaining ground and consumer sentiment remaining soft.

The market is expecting revenue of roughly $11.1 billion for the quarter, flat year on year, an improvement on the 9.3% decline recorded in the same period last year.

Earnings per share, meaning profit divided across all outstanding shares, is expected to land at 29 cents. Last quarter Nike beat on both revenue and earnings, so the bar exists, even if it is not set particularly high.

👟 The Cool Factor Problem

Beyond the financials, Nike has a cultural challenge that balance sheets struggle to capture. The brand that defined athletic aspiration for four decades is working harder than usual to stay relevant.

Its answer, at least partly, is a sneaker called Mind, a shoe focused on mindfulness. Whether a mindfulness sneaker moves the needle on coolness is a question the market will eventually answer, but it is the kind of product that signals a company actively searching for its next identity.

🆕 New Balance Is Having a Moment

While Nike searches, New Balance is sprinting. The 120-year-old brand, once synonymous with sensible footwear for people who prioritize comfort over style, grew sales 19% last year and 180% since 2020.

It has raised average prices by roughly 30% over the past five years, proving consumers will pay a premium for a brand they believe in. It opened 80 new stores last year, aggressively rebuilding physical retail presence at the exact moment Nike was stepping back from it.

New Balance expects to cross $10 billion in sales this year, putting it roughly $2 billion behind Nike's quarterly revenue run rate. That gap is closing, and it is closing fast.

🎯 What to Watch Tuesday

The headline numbers are important, for sure, but the language around China and wholesale recovery will tell the more important story. So grab your two shares and listen for whether management sounds like a team executing a plan or a team revising one.

At $50, Nike is cheap relative to its own history. Cheap and done falling are different things, though.

Off to you : What’s your outlook for Nike? Share your views in the comments!

NKE

SinnSeed | #Nike (#NKE) in 2026 - idea - 26.02.2026🗓 SinnSeed | #Nike (#NKE) in 2026: the tariff window the market hasn’t priced in yet

🕯 As of February 26, 2026, NKE is trading around 64 USD (63.40–65.00), with a market cap of ~94–95 bn USD.

💼 Dividend yield is roughly 2.5% (0.41 USD per share; record date: March 2). At these levels, this is not a story about an “perfect company,” but about skewed expectations and a potentially meaningful re-rating.

📈 Where Nike stands today

Nike is in the middle of a restructuring under CEO Elliott Hill. Management views FY2026 as a transition year: rapid actions to restore sales without permanent discounting, strengthen partner retail channels, refresh the product portfolio, and reduce the share of “aged” inventory. Improvements are starting to show, but the stock price reflects them only partially.

🛒 What looks strong

North America (about 45% of revenue) is recovering noticeably. Partner (wholesale) sales in Q2 grew 8%. Inventory is coming down and the markdown mix looks healthier—an important sign Nike is gradually regaining control over pricing and demand. Product momentum in running, basketball, kids, and Jordan provides additional support.

📉 What continues to weigh

The main weak spot is Greater China: a soft consumer, competition from Anta and Li-Ning, plus consumer nationalism. Nike’s direct digital sales continue to decline (NIKE Digital -14% in Q2). Gross margin in Q2 fell by 300 bps, with a meaningful portion driven by tariffs.

🗺 And importantly: Nike has already baked in about 1.5 bn USD of annual incremental tariff costs in FY2026.

🧮 Regional snapshot (Q2 FY2026, through November 30, 2025)

Total revenue: 12.43 bn USD (+1% YoY reported).

North America: 5.633 bn (+9%).

EMEA (Europe, Middle East & Africa): 3.392 bn (+3% reported).

Greater China: 1.423 bn (-17%).

Asia Pacific & Latin America: 1.667 bn (-4%).

North America and EMEA represent nearly three quarters of the business and remain resilient, while China and other regions continue to drag on the overall picture.

⏱ Core idea for 2026: tariffs may flip from a “headwind” into a “tailwind”

After the US Supreme Court ruled the IEEPA-based tariff framework unlawful, the administration shifted to Section 122 (15%), set to run until July 24, 2026 without Congressional approval. The market reacted emotionally to the headline, but has not fully modeled what may matter more: partial or full removal by the deadline and possible refunds of previously paid duties. Wharton estimates the industry is discussing up to 175 bn USD in potential refunds; for Nike, that could mean the already-modeled 1.5 bn USD cost headwind turns into a one-off cash inflow and a margin boost.

⚖️ The price action supports the underpricing thesis: a short-term pop on the news followed by a pullback—classic “sell the fact,” without a deep scenario repricing.

🎯 NKE price scenarios by end-2026 (from ~64 USD)

🛫 Base case: 75–78 USD (+17–22%). Restructuring stays on track; tariff pressure eases partially. Probability ~55%.

🛫 Bull case: 85–92 USD (+33–44%). Section 122 is removed/neutralized by July and duty refunds reach 50–70% of the modeled 1.5 bn USD. Probability ~35%.

🛫 Bear case: 55–60 USD (-6–14%). Shift to harsher tariff mechanisms plus further deterioration in China. Probability ~10%.

✍️ My midpoint target: 82–85 USD by December 2026 (+28–33%).

💵 Why Nike could outperform peers

Because Nike’s tariff factor is among the largest in absolute dollars, import dependence is high, and margin expectations are already depressed. If the tariff window starts to close, the impact on earnings and valuation could be disproportionately strong.

🗓 Watchlist calendar

Over the next 2–4 weeks: track news on duty refunds and importer lawsuits.

March 19: Q3 earnings (key question: does North America strength persist?).

April–July: peak catalyst window ahead of the July 24 deadline.

⚠️ Key risks

A shift to a tougher tariff framework, no guarantee of full refunds due to legal complexity, and prolonged weakness in China slowing margin recovery.

💡 Bottom line

Nike in 2026 is one of the more interesting retail setups precisely because of the tariff window. The market is still reacting cautiously—and that can be the opportunity. Building a position on pullbacks below 62 USD makes sense, and a move above 80 USD looks achievable if the tariff narrative turns more favorable into July.

NFA | DYOR

With respect to everyone,

Yours, 🫡 #SinnSeed

Bottom Developing-Early Entry200 SMA ever so slightly turning upward after an undecided golden cross.

This all correlates to a low set March 2020

I am making first entry in the right shoulder area. Looking for a first move to resistance.

$NKE: The "Repair Job" in Progress for NIKE👟👟

Nike is currently like a classic sneaker getting dusted down and cleaned up.

It’s not quite "dead money," but it’s definitely not back to full speed yet.

The "Hype" (Why Bulls like it)

The Big Bosses are Buying: CEO Elliott Hill and even Tim Cook (Apple CEO/Nike Board) just dropped millions of their own cash into NYSE:NKE shares. Usually, when the insiders buy the dip, they know something we don't.

Back to Basics: Nike is ditching the "lifestyle" fluff and winning again in Performance Running (up 20% recently!).

North American sales are finally waking up, proving the "Win Now" strategy isn't just a slide deck.

The "Haters" (Why Bears are wary)

China is Still "Meh": Sales in China have been sliding for over a year. It's a tough market to crack right now.

Tariff Trouble: Global trade drama and higher costs are eating into the profits (margins are down about 3%).

The Wait: Management says it’s "middle innings" of a comeback. In other words: bring your patience.

The Bottom Line

If you believe in the "Insider Effect" and the running shoes reboot, this is your entry zone. If you need proof, wait for the $69 breakout.

#NKE #Nike #Turnaround #ValuePlay #TechnicalAnalysis

Trend is your Friend. #NKE is a prime example...fade the bullish moves

look for continuation down

that is going to be the money maker

shorting into resistance

not longing on reversals

NKENIKE ( NYSE:NKE ): Turnaround or a New Wave of Decline?

The Big Picture: Earnings, Insiders, and Technical Resistance

Nike’s Q2 FY26 report shows a modest 1% revenue growth ($12.4B), but the surface growth hides structural decay.

Gross margin plummeted 300 bps to 40.6%, driven by aggressive tariffs and heavy discounting to clear inventory.

Regional & Segment Breakdown:

North America (+1%): Stagnant momentum.

Greater China (-17%): Six consecutive quarters of decline. The "Guochao" trend (preference for local brands) is a structural nightmare for Nike.

DTC (-8%): The "Nike Direct" strategy is faltering, while the brand has already lost crucial shelf space at major wholesalers.

🔎

New All Time Highs - Bullish Price ActionToday the S&P500 made new all time highs.

It was a perfect breakout trend day and breakout.

Today we were able to trim and take profits on some of our long exposure.

We trimmed and sold NASDAQ:AMZN NYSE:SNAP NASDAQ:TEM NYSE:SMR

When the market is giving you all time highs and higher highs its always a good time to pair back longs.

Tomorrow we have some employment data that could gap the market higher.

If we can confirm a weekly chart breakout the probabilities of hitting 7k on spx is very likely.

Run with $NKEOne of those set it and forget it charts.

Patience needed as this is a weekly chart, but i expect a break upward of the failling wedge within a month and a rapid acceleration with a few pullbacks after each target is reached.

$79, 98, and 121 targets over the next 8 months.

NKE NIKE Options Ahead of EarningsIf you haven`t sold NKE before the previous earnings:

Now analyzing the options chain and the chart patterns of NKE NIKE prior to the earnings report this week,

I would consider purchasing the 69usd strike price Calls with

an expiration date of 2025-12-19,

for a premium of approximately $2.51.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

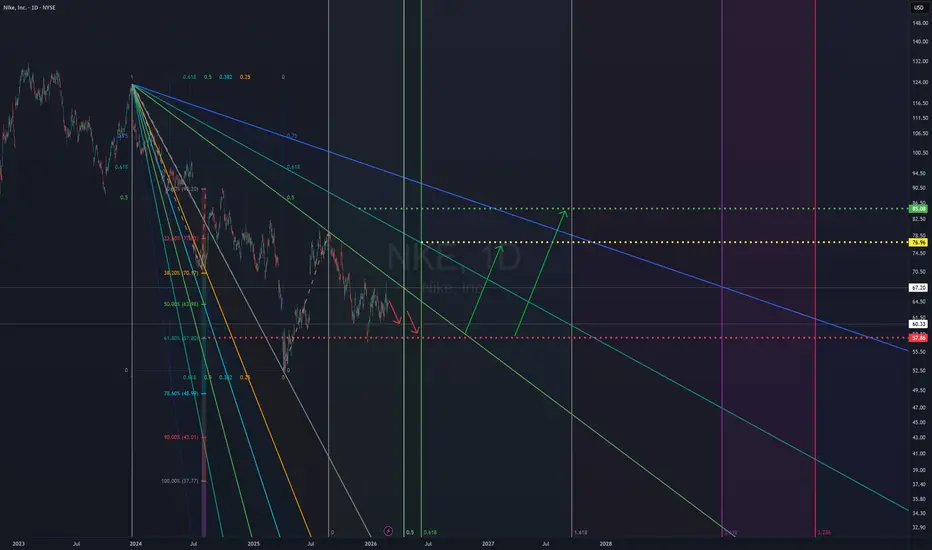

Nike is reaching trough lands soon ! Or not & W crash more !61% Retracement from all time low "IPO" to "ATH" is in the 60ish region. MKTS permitting & unless we are about to crash just like 1929 as some Elliottsions suggest then we are about to have a trough in Q1/Q2 of 2025 .!

NKE long idea Long CALLS NKE at 68. 6 weeks expire. SMT in the lows with SP500, this pattern indicates strong demand on NKE.

December 2025 is Hurst's 9 Years Cycle!Margin of Error "Adjusted" on the chart:

9 Years, 4.5 Years and 18 Months !

1: September 2025 is our early trough

2: 2027 is our late trough

3: Or we are having one right now !

Nike by April 2025 we should have break out or breakdown !101 Trend lines analysis. By April we should could/might reach the Red line in which we will have a break out to a new ATH in the next years or so or a break down to the 40ish/50ish region.!

Nike's 1984 Vs 2000 Major Trend lines The 1984 Major and historical Trend line is already broken with 3 candles below, technially

this is a valid and confirmed breakdown.

The 2000 Major and historical Trend line is hanging by $5 give or take $66 -+ is the support for the TL.

NIKE — $31–$11 bottom | Before SuperCycle Wave 3 hits ~$1000⚡ NKE: Micro Wave 4 Bounce Before the Final Flush 👟🔥

Nike ( NYSE:NKE ) has been in a SuperCycle Wave (2) correction since topping near $179 in 2021. This isn’t a collapse — it’s a structured reset that should run into 2027 , forming a large ABC correction before the next SuperCycle Wave (3) bull phase begins.

Right now, price action is inside a micro Wave 4 move within the ongoing Wave A. Micro waves 1, 2, and 3 have completed, and waves A and B of this current wave 4 are also done. What’s likely next is a short-term bounce toward $82 , where equal highs and liquidity sit, before a final Wave 5 decline finishes Wave A around the 0.236 Fibonacci retracement near $31 .

From there, expect a Wave B rebound followed by Wave C down toward the 0.382 retracement around $11 , which could complete the full SuperCycle Wave (2) correction. That zone may become the macro accumulation area ahead of the next explosive SuperCycle rally.

The $82 region aligns with a liquidity grab in Smart Money terms — a trap for breakout buyers before price descends into the deeper $31–$50 institutional value range , matching demand zones from 2016–2018.

This phase is less about panic and more about patience. Once the 2021–2027 correction ends, Nike could begin a multi-year rally that redefines its valuation.

The swoosh isn’t breaking — it’s recharging for its next leap. 👟⚡

#NKE #Nike #ElliottWave #SmartMoneyConcepts #WaveTheory #Fibonacci #PriceAction #MarketCycle #TechnicalAnalysis #TradingViewAnalysis #StocksToWatch

Global Brand Power Driving Growth Opportunity: BUYBuy Reason: Nike’s strong brand presence, global market penetration, and innovation in sportswear position it for steady revenue growth and resilience amid market fluctuations. Its expanding digital sales and product innovation make it attractive for long-term investors.

NKE Pullback-I'm Buying the DipNike (NKE) is under pressure — post-earnings volatility, macro noise, and sentiment all weighing in. But for swing traders, this looks like a textbook accumulation setup.

📌 Entry Zones I’m Targeting:

🔹 $70.00

🔹 $65.00

🔹 $60.00

Profit Targets (Taking wins before 88):

✅ $78.80

✅ $82.50

Let the market come to you — no chasing, just precision.

💬 Drop your thoughts below — are you buying NKE here or waiting for blood?

Disclaimer: This post is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any securities. Always do your own research and consult with a licensed financial advisor before making any investment decisions. Trading involves risk, and past performance is not indicative of future results

$NKE Inverse Head and Shoulder $117 to gap fillThe chart is currently forming a classic Inverse Head and Shoulders pattern, which is a bullish reversal setup. The left shoulder and head have already been established, and the right shoulder is in development, suggesting a potential breakout to the upside. The neckline resistance appears to be around the $73-$85 range. A confirmed breakout above this level could trigger a measured move toward the $117 gap fill, which aligns with a previous price gap and serves as a logical target for bullish momentum.

Key technical highlights:

Target Price: ~$117 (gap fill zone)

If volume confirms the breakout above the neckline, this setup could offer a strong risk/reward opportunity for traders. Keep an eye on RSI and MACD for confirmation of bullish momentum.

Nike 1W - Just buy it?Nike is showing signs of a reversal after a prolonged downtrend, holding the key buy zone at 69.52, which aligns with the 0.618 Fibo retracement. The breakout of the descending channel adds weight to a structural shift, with the first target seen around 97.63, where the 1.618 Fibo extension and a major resistance zone converge. A successful breakout above this level would open the path toward 125.73, coinciding with the MA200 and a significant volume cluster. While the MA50 still hovers under price, suggesting caution in the short term, the overall structure points toward a bullish scenario.

Fundamentally , Nike remains solid, supported by recovering consumer demand and cost optimization, while its strong brand and institutional interest create a backdrop for sustained growth.

The tactical outlook favors a bullish continuation as long as price holds above the 69.5 zone, with upside targets at 97.6 and 125.7.

If buyers manage to maintain momentum, the market might just rewrite Nike’s slogan: “Just buy it.”

Nike - This is the bottom!💉Nike ( NYSE:NKE ) creates the bottom now:

🔎Analysis summary:

More than four years ago, Nike created its previous all time high. We have been witnessing a downtrend ever since and a correction of about -70%. But with the recent retest of an important horizontal structure and bullish confirmation, Nike is about to create a potential bottom.

📝Levels to watch:

$65, $80

🙏🏻#LONGTERMVISION

Philip - Swing Trader

Nike Looks Ready — A Smart Time to Consider InvestingOn the monthly chart, NIKE has been in a downtrend since November 2021, but the signs are pointing toward a potential trend reversal. Here's why I believe the bottom may already be in:

✅ MACD Histogram shows a strong positive divergence, signaling weakening bearish momentum.

✅ The RSI downtrend line has been broken and successfully retested, confirming bullish strength.

✅ A clear hammer candle has formed at a historical wide support zone, showing strong demand.

Now, price is facing three consecutive resistance levels — and with each breakout, the next zone becomes the new target, (87.5 → 102 → 122).

The structure suggests a step-by-step move higher if momentum holds. Keep an eye on the breakout above the descending trendline — that’s where things could accelerate.

NKE - Fallen-Angel reversal + weekly divergence - LongNKE - Nike from Smart Money divergent scanner back on the 15th of April. It's also a fallen angel pattern; it's rolled up beautifully and hitting its first target. Some small insider buying.

$NKE Tradespoon – Long Entry $76.39Tradespoon model generated long signal for NYSE:NKE . Predicted range: $76.39–$80.79. Trend: +2.78%. NYSE:NKE