Micron Technology - Heading for another -50%!☠️Micron Technology ( NASDAQ:MU ) is perfectly following all structure:

🔎Analysis summary:

I remember literally everyone hating on me calling the top on Micron Technology. Yet just two weeks later, we are witnessing a harsh -30% correction. Looking at the higher timeframe this is just the beginning and Micron Technology can correct another -50%.

📝Levels to watch:

$150

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

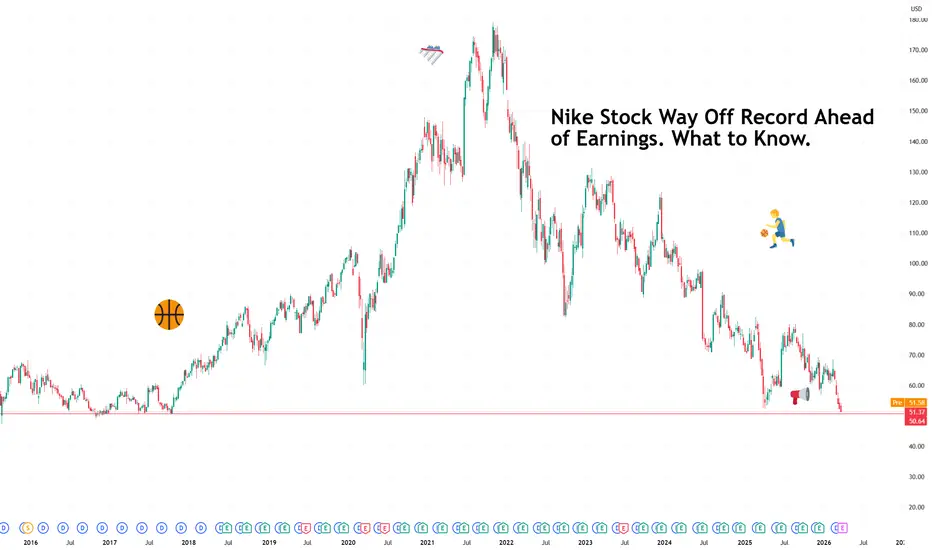

Nike Stock Way Off Record Ahead of Earnings. What to Know.There is a particular kind of corporate humbling that comes not from collapse but from irrelevance creeping in at the edges.

Nike NYSE:NKE is still the world's largest sportswear brand, still moving tens of billions in revenue, still on the feet of more athletes than any other company on earth.

And yet at around $50 a share, nine-year lows, off 70% from its 2021 peak, the stock is asking a question the company has to answer on Tuesday: So how’s that reset going? (insert "well we’re waiting.gif")

The earnings calendar rolls on with Nike’s earnings day next .

📉 How Did We Get Here?

Nike's November 2021 high of $178 looks almost fictional from today's vantage point. The shares are lower by more than 20% this year alone and have spent the past several months hovering near levels last seen when athleisure was still a novelty.

The company is in the middle of what it calls a business reset , refocusing on wholesale partnerships after a years-long push toward selling direct to consumers that did not deliver the margins management had anticipated.

Wholesale means selling through retailers like Foot Locker rather than exclusively through Nike's own stores and app. The retreat is sensible but the execution has been choppy, and the market has been keeping score.

🌍 Three Problems, One Earnings Call

Investors heading into Tuesday's report are watching three specific pressure points.

Europe is slowing. Consumer confidence across the continent has softened, and discretionary spending, the kind that goes on premium trainers, tends to be the first casualty when household budgets tighten.

The US wholesale business, the very channel Nike is trying to reinvigorate, remains unhealthy. Rebuilding retailer relationships after deprioritizing them takes time, and the inventory and shelf-space dynamics are still normalizing. All the while profits are slumping .

Outside the tariff woes from a year ago , China continues to disappoint. The post-pandemic recovery that Nike and many other consumer brands were counting on has been more stubborn than anticipated, with local competitors gaining ground and consumer sentiment remaining soft.

The market is expecting revenue of roughly $11.1 billion for the quarter, flat year on year, an improvement on the 9.3% decline recorded in the same period last year.

Earnings per share, meaning profit divided across all outstanding shares, is expected to land at 29 cents. Last quarter Nike beat on both revenue and earnings, so the bar exists, even if it is not set particularly high.

👟 The Cool Factor Problem

Beyond the financials, Nike has a cultural challenge that balance sheets struggle to capture. The brand that defined athletic aspiration for four decades is working harder than usual to stay relevant.

Its answer, at least partly, is a sneaker called Mind, a shoe focused on mindfulness. Whether a mindfulness sneaker moves the needle on coolness is a question the market will eventually answer, but it is the kind of product that signals a company actively searching for its next identity.

🆕 New Balance Is Having a Moment

While Nike searches, New Balance is sprinting. The 120-year-old brand, once synonymous with sensible footwear for people who prioritize comfort over style, grew sales 19% last year and 180% since 2020.

It has raised average prices by roughly 30% over the past five years, proving consumers will pay a premium for a brand they believe in. It opened 80 new stores last year, aggressively rebuilding physical retail presence at the exact moment Nike was stepping back from it.

New Balance expects to cross $10 billion in sales this year, putting it roughly $2 billion behind Nike's quarterly revenue run rate. That gap is closing, and it is closing fast.

🎯 What to Watch Tuesday

The headline numbers are important, for sure, but the language around China and wholesale recovery will tell the more important story. So grab your two shares and listen for whether management sounds like a team executing a plan or a team revising one.

At $50, Nike is cheap relative to its own history. Cheap and done falling are different things, though.

Off to you : What’s your outlook for Nike? Share your views in the comments!

EXXON MOBIL can almost double within 3 years.Exxon Mobil (XOM) has started a new Bull Cycle, one sequence that is recurring within its 58-year trading history. Helped to a large extent by the current geopolitics (U.S. - Iran war), the price is extending this month a rally that started after the April 2025 Low on the 1M MA50 (blue trend-line).

Historically it looks like the we are at least half-way inside a Bull Cycle like the previous one where in January 2022 the Ukraine - Russia war started. We believe that as long as the 1M MA50 supports, the market should complete at least a +218.50% rally from the April 2025 Low, which is historically the minimum Bull Cycle it had % wise.

This gives a $310 Target on a 3-year horizon. Even when the 1M RSI hits the 87.00 Resistance, it historically means that the Bull Cycle isn't over yet.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

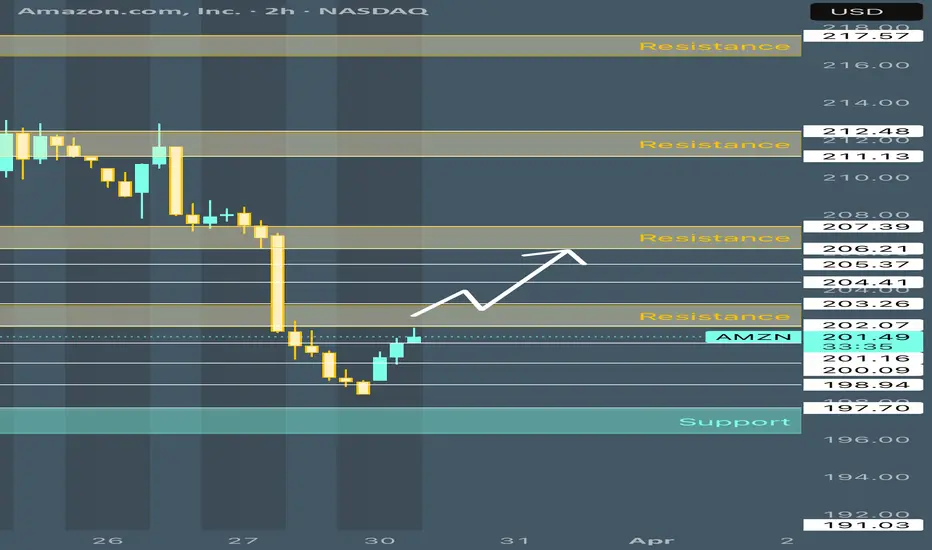

Possible AMZN setups**PLAY OF THE DAY**

**AMZN**

Watching for two different scenarios here depending on what we see across the markets as a whole. Both setups looks like they have great potential to finally get us back on track with some great options trades this week!

**SHORT SETUP**

**ENTRY** - 202-202.75

**SL** - over 203.25 (if entering closer to 202 then SL over 202.75)

**PT** - 201.15 / 200 / 199

**LONG POSITION**

**ENTRY** - over 203.25

**SL** - under 202.75

**PT** - 204.35 / 205.25 / 206

@everyone

TSM – The Make or Break Zone for BullsTSM is approaching a strong support zone, where structure aligns perfectly with the lower bound of the rising channel.

This intersection creates a high-probability reaction area.

⚔️ As long as bulls defend this level, the overall trend remains bullish, and we can expect continuation toward higher highs.

Lose this zone… and the structure starts to weaken.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

NDVA weekly view. Headline risks.Nvidia has been pulling back from the $190 level since the start of the war and is currently sitting below the 200d sma. Big tech is under pressure from rising oil prices, a stronger dollar and a possible self-induced recession if oil prices remain elevated. I have outlined two balanced area's on the chart; Balance Area #1 and Balance Area #2. I still have a bullish bias on the chart as long as price stays in Balance Area #2. Since late 2022 NVDA stock does not fall below the 40's RSI level very often on the weekly. Therefore there could be a chance we get an oversold bounce soon. If this occurs then I believe we could bounce back up to the 200d ma ($179)- roughly a 7% move. If we do and it rejects then I think it's possible we reject all the back down to the bottom of Balance Area #2 ($149). Or, If you take the top of Balance Area #1 and measure the percent move down to the bottom, it is 41%. The price has moved down 19% since the ATH. If you add another 21% to total the 41% move from Balance Area #1 you get $122; falling outside of Balance Area #2 and about 50% into Balance Area #2. I don't think NVDA is a trade unless it can reclaim the 8d sma (approx. $174).

You might be surprised by what I’m about to say now. $RIG🚨 You might be surprised by what I’m about to say now.

A few weeks ago, I took a long position, and it’s already in solid profit.

Here’s the reasoning behind the trade.

The oil era is not ending, it is evolving.

ExxonMobil and OPEC now expect global oil demand to continue growing well beyond 2030, potentially even past 2050. Even the IEA and BP , once forecasting peak demand, have revised their outlooks upward.

The key question is no longer demand.

It’s supply.

The Critical Shift: Deepwater

Most conventional onshore fields have already peaked.

Future production growth is increasingly dependent on:

Offshore deepwater

Ultra-deepwater basins

These are long-cycle, capital-intensive projects with high barriers to entry — but once operational, they deliver stable production for decades.

The Underappreciated Supply Constraint

Around 2020, shipyards effectively stopped building new deepwater rigs.

Why?

Because the prevailing assumption was that:

NSE:OIL demand was about to peak

The energy transition would reduce long-term need

Deepwater capacity would become obsolete

As a result, newbuild orders dried up.

This creates a structural bottleneck:

If demand for offshore drilling increases, supply cannot quickly respond.

The Long-Term Swing Opportunity: NYSE:RIG

NYSE:RIG is one of the very few companies with meaningful exposure to ultra-deepwater rigs, and it stands to benefit significantly if oil sustains above $85.

Above that level, offshore projects become far more economical, and profitability for deepwater drillers can expand rapidly.

Technically, oil’s monthly chart is forming a large wedge. These long-term compressions typically resolve with expansion, often toward the midpoint first. That alone would project oil into the $85 zone.

Longer term, new all-time highs in AMEX:USO are not unrealistic. Inflation alone shifts nominal price regimes over decades. In the 1960s, oil traded below $5 per barrel. Even without severe supply-demand imbalances, oil is likely to make new nominal highs over time.

This position is held in a separate long term account so it doesn’t drain trading focus.

Has Micron just formed a top?!Micron has clearly formed an evening doji formation, which is a bearish formation signalling a top, turnaround.

This is a monthly chart you are looking at, which candle closes tomorrow, so most likely won't change that much.

I like to invest into stocks for long term or make swing trades, I am not shorting MU here, as I only do long swings, just a simple technical analysis.

Don't fall into the overhype of Memory stocks or AI stocks, despite Micron having a very good quarter, a 50 EMA visit is a common thing for many stocks, Micron included, as you may see in the chart.

Ex-dividend date is also today, which should have a minor negative impact on the price also.

My target would be 50 monthly EMA, the orange one.

RKT: Is Set For A BounceEyes on RKT ladies and gentlemen . Is set up for a bounce.

Finally is coming to Papa. First buy order Now and 2nd 1/2 buy order at the 2nd supply zone

Play it right.................Play it safe.................Play it The Numberfive Way.

Boost...............Follow.................Share...................Comment.

CoreWeave Gains on Bank of America Coverage InitiationCoreWeave (NASDAQ: CRWV) Gains on Bank of America Coverage Initiation with Buy Rating and $100 Price Target

Shares of CoreWeave (NASDAQ: CRWV) edged approximately 1% higher in Tuesday morning trading following the resumption of coverage by Bank of America, which assigned the stock a Buy rating alongside a $100 price target. The bullish call from the investment bank reflects a positive outlook on the company’s expanding customer base and the sustained, robust demand for artificial intelligence infrastructure.

Analyst Tal Liani, who authored the research note, argued that CoreWeave is well-positioned to capture a growing share of the estimated $79 billion AI infrastructure-as-a-service market. Liani highlighted several key factors supporting this thesis, including persistent demand for high-performance computing power, the company’s development of software specifically tailored to AI workloads, and its strategic partnerships with industry heavyweights such as Nvidia and OpenAI.

In addition, Liani pointed to the emergence of agentic AI—a category of AI systems capable of autonomous decision-making and action—as a trend that could further amplify infrastructure requirements. As agentic AI applications become more widespread, he noted, the resulting increase in demand may help keep computing capacity constrained, potentially sustaining favorable pricing dynamics for infrastructure providers like CoreWeave.

The analyst also offered a long-term perspective on supply and demand imbalances in the sector. Liani expects capacity shortages across compute resources, power availability, and related infrastructure to persist for years, with no meaningful relief anticipated before 2029. This extended period of constrained supply, he suggested, could continue to benefit companies that have secured early access to critical resources and established strong partnerships.

CoreWeave’s Recent Share Performance and Valuation Considerations

CoreWeave has attracted considerable investor attention in recent months, particularly following its public market debut. The stock most recently closed at $74.41, reflecting a complex short-term performance picture. While the shares recorded a modest gain on the day of the Bank of America note, they have experienced negative momentum over the past week and over the three-month period, indicating some near-term volatility.

Zooming out, the broader performance metrics show a more nuanced trajectory. CoreWeave’s share price has delivered a 4.66% return over the past seven days and a 17.92% return over the past 90 days. On a year-to-date basis, the stock is up 6.19%. Despite these positive returns over certain time frames, analysts note that short-term momentum has shown signs of fading, prompting questions about whether the current pullback represents a buying opportunity or whether the market has already priced in expectations for future growth.

A Divergence in Narratives: Valuation and Future Growth

The company’s financial profile adds another layer of complexity to the valuation debate. CoreWeave has demonstrated impressive revenue growth, yet it continues to report operating losses—a common characteristic among rapidly scaling infrastructure companies that are investing heavily in capacity expansion ahead of profitability.

Amid this backdrop, a notable divergence has emerged in how market participants assess CoreWeave’s valuation. According to Vestra, a widely followed analytical platform, one prevailing narrative suggests that CoreWeave is significantly undervalued. Vestra’s model estimates the company’s fair value at $133.12 per share, representing a substantial premium to the recent closing price of $74.41. This valuation thesis builds a detailed case around the sustained growth of AI infrastructure demand and the capital-intensive nature of the business, arguing that CoreWeave’s current market price does not fully reflect its long-term potential.

For investors weighing their options amid CoreWeave’s recent pullback, the current environment may present an opportunity to evaluate a broader selection of companies operating within the same AI infrastructure theme. A curated basket of 35 AI infrastructure stocks—all of which are positioned to benefit from the same underlying trends in computing demand, power requirements, and data center expansion—offers one lens through which to compare relative value and growth prospects across the sector.

MSFT LEAPs Showing Strong Institutional Bullish Flow-Trade idea*.

Last week we were discussing how NASDAQ:MSFT price action was likely to first sweep the remaining liquidity sitting in the low 350s before we could expect any meaningful reversal or continuation.

Well, here we are, the price has come very close to tapping exactly those liquidity levels, and now we’re starting to see early signs of institutional interest stepping in.

Today, Monday March 30, 2026, the LEAPs options flow is sending a clear long-term bullish signal. The December 18, 2026 $575 Call stands out as the single highest volume strike across all LEAPs, with over 200,129 contracts traded today alone.

This concentrated call buying at high strikes in the long-dated LEAPs is classic smart money & institutional positioning. Institutions appear to be loading up aggressively, suggesting they may know something the broader market doesn’t, or at least they have high conviction that the current weakness and liquidity sweep in the 350s is a buying opportunity rather than the start of a deeper decline.

Are we approaching a local or intermediate bottom in NASDAQ:MSFT ?

The LEAPs flow today is leaning heavily toward "yes"

Watching this setup very closely. Smart money positioning deserves attention.

Week 14 of 52 — Even defensive stocks are breaking downWhile most traders are focused on high-beta names, something bigger is happening under the surface.

UnitedHealth Group — one of the strongest defensive stocks in the market — is breaking down.

This is not just a pullback.

This is a shift in confidence.

The Setup

When defensive stocks start losing key levels, it usually means one thing:

👉 The market is no longer looking for safety

👉 Liquidity is moving… or leaving

The Real Question

Everyone is asking where to buy tech…

But maybe the real signal is here:

👉 Why is money leaving safety?

Entry Zone:

Market Price (~260 area)

$230 – $220

$200 – $190

Target:

$285

$310

$340+

This is not just a healthcare stock setup.

This is a market sentiment signal disguised as a trade.

This is not financial advice.

Do your own research and manage your risk accordingly.

Broadcom: ‘Death Cross’ Coming?Broadcom has gone nowhere since September, and now traders may think its trend is reversing.

The first pattern on today’s chart is the 50-day simple moving average (SMA) nearing a potential “death cross” below the 200-day SMA. That may suggest its longer-term direction is turning bearish.

Second, the chip giant just had its lowest weekly close since the end of August. Is support breaking?

Third, AVGO made a lower peak in March versus January. Both were well below the previous all-time high from December. Those lower highs may be consistent with the conclusion of a topping pattern.

Next, the 8-day exponential moving average (EMA) is below the 21-day EMA and MACD is falling. Those signals may reflect short-term bearishness.

Finally, AVGO is an active underlier in the options market. (Its average daily volume of 236,500 contracts ranks 14th in the S&P 500, according to TradeStation data.) That could help traders take positions with calls and puts.

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. If you're born to trade, we could be for you. Learn more here about TradingView’s Broker of the Year!

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com . Visit www.TradeStation.com for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com .

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

FedEx May Face HeadwindsFedEx has enjoyed a strong advance, but now the delivery stock may face headwinds.

The first pattern on today’s chart is the failed rally on March 20 after earnings beat estimates. Given the jump in energy prices and risks of slower economic growth, investors could be shifting their focus to macro risks.

Second, FDX bounced at $346.01 before the report but has quickly returned to the same level. Could that support level break?

Third, the 8-day exponential moving average (EMA) is under the 21-day EMA and MACD is falling. Those signals may reflect growing short-term bearishness.

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. If you're born to trade, we could be for you. Learn more here about TradingView’s Broker of the Year!

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

TSLA - 2H Bullish DivergenceOn the 2H timeframe, Tesla has formed a bullish divergence worth paying attention to heading into today's session.

The divergence was established with a lower low in price action paired with a higher low on the RSI which is a classic bullish divergence signal. The price low also swept the prior lows, which is an encouraging sign that stop losses have been triggered and liquidity collected. Adding to this, the 2H RSI is bouncing right off oversold conditions (30).

Of course, today is likely to be a volatile session with several headlines demanding attention. But in these early trading hours, TSLA is showing early signs of strength for a potential move back toward the top of the falling wedge pattern around $385.

Coinbase Short-term analysis | Trading and expectationsNASDAQ:COIN

🎯 Price was rejected at the descending trend line resistance, suggesting we lose the High Volume Node and head lower.

📈 Daily RSI is approaching oversold again

👉 Analysis is invalidated above wave (4), keeping the bullish move alive

MSTR Short-term analysis | Trading and expectationsNASDAQ:MSTR dropped hard in wave Y of 4, but looks complete, reclaiming the daily pivot. This is now under threat once more as price is testing as support.

📈 Daily RSI hidden bearish divergence is playing out, with plenty of room to fall

👉 Continued downside has a target of the S2 pivot, $83.47

Nvidia: Potential BreakdownNvidia has been stalling for months, and now some traders may think it’s breaking down.

The first pattern on today’s chart is the potential double top between the peaks of November 20 and February 25.

Second, NVDA dropped sharply after that potential reversal pattern. It retraced about half the move before stalling, which may confirm its direction has turned bearish.

Third, the mid-March closing highs were also near the February 26 closing price of $184.89. That could indicate resistance has been established around a prior low.

Fourth, the chip giant spent most of last week under its 200-day simple moving average -- a potential sign of longer-term bearishness.

Fifth, the 8-day exponential moving average (EMA) is below its 21-day EMA. MACD is also falling. Those patterns may reflect short-term bearishness.

Next, the stock bounced a few times near its November 25 low of $169.55. However, it closed under that level on Friday. Is support breaking?

Finally, NVDA is a highly active underlier in the options market. (Its average daily volume of 2.9 million contracts ranks first in the S&P 500, according to TradeStation data.) That could help traders take positions with calls and puts.

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. If you're born to trade, we could be for you. Learn more here about TradingView’s Broker of the Year!

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

Options trading is not suitable for all investors. Your TradeStation Securities’ account application to trade options will be considered and approved or disapproved based on all relevant factors, including your trading experience. See www.TradeStation.com . Visit www.TradeStation.com for full details on the costs and fees associated with options.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com .

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

Can Science Build a $1 Trillion Moat?A Pharmaceutical Titan in Full Transformation

Eli Lilly and Company is undergoing one of the most consequential transformations in modern pharmaceutical history. No longer simply a drug manufacturer, the company has evolved into a high-tech industrial platform, one that fuses cutting-edge biological science with autonomous manufacturing systems and artificial intelligence. At the center of this revolution is tirzepatide, a first-in-class dual GIP and GLP-1 receptor agonist marketed as Mounjaro (diabetes) and Zepbound (obesity). This molecule has become the engine of Lilly's financial ascent, delivering 23.6% average weight loss in clinical trials and outperforming rival semaglutide by 47% in relative weight loss. In 2025, the company reported revenue of $65.2 billion, a performance that drove a 40% total shareholder return, and issued 2026 guidance of $80 to $83 billion, representing a projected year-over-year increase of 23% to 27%. With a market capitalization that recently crossed the $1 trillion threshold, Lilly's rise is not a speculative story; it is a structural, multi-domain rearchitecting of the global healthcare economy.

Manufacturing Moat and Geopolitical Realignment

To sustain its dominance, Lilly is constructing a manufacturing fortress that smaller competitors cannot replicate. The company has committed over $55 billion to 13 new production sites worldwide, including a $3 billion facility in Katwijk, Netherlands, featuring fully automated "dock-to-dock" systems, and a €400 million biopharmaceutical plant in Limerick, Ireland. On the horizon, its next-generation oral GLP-1 drug, orforglipron, could be priced as low as $149 per month, a move that would fundamentally reprice the entire obesity treatment category. Simultaneously, Lilly is navigating the geopolitical turbulence created by the BIOSECURE Act, which threatens to restrict partnerships with Chinese biotechnology suppliers by 2032. With Chinese firms representing 13% of global active pharmaceutical ingredient manufacturers, the company is actively reshoring production to allied nations, a costly but strategically vital shift. These capital-intensive decisions are not merely defensive; they are offensive moves designed to lock out rivals and create a decade-long supply chain advantage.

AI, Pipeline Innovation, and Patent Durability

Lilly's competitive edge extends deep into the future through its integration of artificial intelligence and a robust pipeline of next-generation molecules. A $1 billion partnership with NVIDIA has yielded AI-powered "factories" capable of analyzing complex protein structures, while a $2.75 billion collaboration with Insilico Medicine is compressing drug discovery timelines from years to months. The pipeline's crown jewel is retatrutide, a triple agonist targeting GIP, GLP-1, and glucagon receptors, which demonstrated 16.8% weight loss in just 40 weeks without a plateau, a signal of even greater potential. On the intellectual property front, tirzepatide is shielded by 23 separate U.S. patents, with an estimated generic launch for Zepbound not until 2039, providing over a decade of high-margin exclusivity. Policy shifts, including the CMMI BALANCE Model that caps Medicare out-of-pocket costs for GLP-1 drugs at $50 monthly starting in 2027, further expand the addressable population, turning weight-loss medications into affordable standards of care for millions.

Risks, Valuations, and Analyst Consensus

Despite its commanding position, Lilly is not without meaningful risks. Realized prices fell 7% in Q4 2025 even as volume surged 50%, signaling intensifying pressure from pharmacy benefit managers demanding larger rebates. Competitive threats are materializing from Structure Therapeutics, Roche, and AstraZeneca, particularly around the emerging "muscle preservation" standard expected to define the next generation of obesity trials in 2027. A 16% year-to-date share price decline in early 2026 has created what many analysts view as a compelling entry point: over 91% of covering analysts maintain a "Buy" rating, with an average price target near $1,223 per share, and a PEG ratio of 0.41 that suggests the stock remains undervalued relative to its growth trajectory. The lone dissenting voice, HSBC, which issued a "Reduce" rating with an $850 target, argues that consensus market size estimates above $150 billion may be too optimistic. Yet with revenue growth at 4x the S&P 500 average and 2026 non-GAAP EPS guidance of $33.50 to $35.00, Eli Lilly remains, by most metrics, the highest-conviction large-cap opportunity in the global healthcare sector.

Expecting a bounce on Google this weekExpecting a bounce on Google this week as RSI is sold on daily. Its supported by trendline on the RSI and also in the support channel. As long it hold up $260, i am expecting a bounce towards $290-300

NVDA after last week selloff — how I’m looking at tomorrow (Mar

1H view

I’m starting with the 1H and this one is clean… trend is clearly down.

You had that push up near ~180–182, then it rolled over hard and since then it’s just:

* lower highs

* steady sell pressure

* no real bounce structure

Now price sitting around 166–167, which was a prior support zone… but like the others, once it breaks, it usually turns into resistance later.

So for me, key zone above is 170–174. That’s where sellers showed up before.

15M view

Zooming in, this looks even more controlled.

You can see:

* breakdown

* small bounce

* continuation lower

Now it’s just grinding sideways near lows around 165–167.

That’s not strong buying… that’s more like sellers pausing.

No real CHoCH or reclaim yet. Until that happens, I’m still leaning downside.

GEX / options positioning

This is where it gets important.

There’s heavy negative gamma below:

* 165

* 160

* lower levels stacked

That means if price starts slipping again, it can accelerate fast.

Above price:

* big resistance around 180 area (call wall / HVL zone)

* nothing strong in the middle to support a bounce

So upside doesn’t have much fuel right now, but downside has room.

How I’d approach tomorrow

If price pushes into 170–174

This is my main spot.

If it pops there and slows down, I’d expect sellers to step in again.

From there I’m watching for:

* 166 retest

* then 162–160

If it breaks below 165 early

Then I’m not trying to catch bottom.

That opens:

* 162

* then 160

And with negative gamma, this can move quick.

If bulls want control back

They need to reclaim 174+ and hold above it.

Not just a wick… I want acceptance.

If that happens, then maybe we see:

* 178

* possibly 180

But right now, nothing on the chart says that yet.

How I’m thinking about it

Same story as the rest of the market.

This doesn’t look like accumulation… it looks like:

* breakdown

* pause

* likely continuation

So I’m keeping it simple:

* short into resistance

* or wait for real reclaim before thinking long

Anything in between is just chop.

MSFT After That Drop — what I’m watching for March 291H view (bigger picture)

When I look at the 1H, it’s still pretty clear… we’re in a downtrend.

Price keeps getting rejected at lower highs, and that 358–360 area is where sellers showed up again. That zone matters now. Every time price gets there and fails, it just confirms sellers are still in control.

I don’t see any real shift yet. No strong reclaim, no higher high… just a bounce that got sold.

So for me, unless price gets back above 360 and holds, I’m still thinking downside first.

15M view (what it’s doing now)

On the 15M, it’s just sitting near the lows, kind of grinding sideways between ~350 and 356.

This type of action usually tricks people into thinking it’s base building… but in a downtrend, it’s often just a pause before continuation.

You can see:

* Bounces are weak

* No real momentum up

* Structure still making lower highs

So I’m treating this as compression, not reversal (yet).

GEX side (this is the part people miss)

Now this is where it gets interesting.

There’s a lot of negative gamma sitting below price (around 350, 340, etc). That means if price starts dropping, dealers are forced to sell more to hedge.

That’s why these moves don’t just drift down… they accelerate.

Also notice there’s not much strong positive gamma nearby to act as support. So there’s not much “cushion” under price right now.

That’s why I’m not trying to catch bottom here. It’s just not that type of environment.

How I’d approach tomorrow

If price pushes up into 356–358 and stalls

I’d be watching for rejection there. That’s basically the same area that’s been failing.

If that happens, I’d lean bearish with targets:

* 350 first

* then 346

* and if things get aggressive, 340

If it keeps breaking lower, the move can get fast because of the gamma setup.

If bulls actually step in

For me, they need to prove it.

I want to see price reclaim 360 and stay above it, not just spike and fade.

If that happens, then I’d look toward:

* 365

* maybe 368

But until that happens, I’m not assuming upside.

How I’m thinking about it

Right now this doesn’t feel like a bottom. It feels like the market is just pausing after a strong move down.

So I’m not trying to be early. I’d rather wait for either:

* rejection at resistance (for continuation), or

* a clean reclaim (for reversal)

Anything in the middle is just chop.

Just how I’m reading it from the chart and positioning. Trade it your way and manage risk.