Crude Oil - When Elvis Leaves The Building ($68)Geopolitics suggests a temporary halt to the war in Iran.

Is it true?

We can't count on this "news".

Let's rely on our pitchforks/median lines:

Price is nagging at the orange L-MLH multiple times now.

The last tiny support is the red dotted line - the Sliding-Parallel.

This is the door to lower prices. If "Elvis" walks through that door, we will probably see a waterfall of stop-runs and more shorts piling in.

My first target is the 50% line of the whole projected move.

Then the warning line.

And by the way: The WL1 builds a compelling confluence with the GAP from March for a target.

Let's see if Elvis plays a smooth love song, lifting crude prices to new highs, or if he slaps his guitar like a real rock 'n' roller from the good old days and sends prices roaring down to our target levels.

Best

Emilio

Light Crude Oil Futures

No trades

In-depth trading ideas

Crude: One More Push To 104-110, Then Lower?Crude oil had a pretty sharp drop yesterday after Trump said the US was in talks with Iran, but it is still not really clear whether this is confirmed or just something that temporarily pressured the market.

Looking at the price action, we still think that a higher degree correction will continue, as we have five waves down from the 120 spike. In our view, we are now in the middle of a higher degree A-B-C decline, therefore, oil could resume !!!BUT!! after wave B is completed, which is still in an intraday corrective recovery phase.

Resistance is seen around 104 to 107, and possibly even up to 110, which also aligns with the 78.6% Fibonacci level. That zone could act as an area from where weakness resumes, but after another short term push higher as presented on the 4h chart where recent sell-off stoped at 61.8% Fib support.

However, if price continues to move sideways instead of pushing higher, then a triangle could also develop here, but for now thats an alternate scenario. So its not the primary view, as the rebound from the March 10 low looks like an impulsive wave A so zigzag fits better to this structure.

Crude Oil Enters Key Reversal ZoneCrude oil has rallied sharply from the March 10th low near 75, unfolding in what appears to be at least a three-wave recovery, as outlined in our previous analysis. With the latest price action, the market has now pushed back above the 100 level and is testing the prior wave “a” high, signaling entry into a critical resistance and potential reversal zone.

This key zone is defined between 104.70 and 107.70, with an extension toward 110 also acting as a significant barrier, particularly as it aligns with the 78.6% Fibonacci retracement. Given this confluence of resistance, the market may be approaching exhaustion, opening the door for a bearish turn—potentially as early as this week.

From an Elliott Wave perspective, the current structure supports the view that a larger corrective phase is still in play. As long as crude oil remains below the 120 level, the outlook favors the development of a strong impulsive move to the downside. Such a decline would likely represent part of wave E, as illustrated on both the daily and monthly timeframes.

A renewed move lower in crude oil could have broader intermarket implications. In particular, it may provide support for equity markets, while contributing to a slowdown in the U.S. dollar’s momentum.

Crude Oil Pushing HigherThe crude oil market has undergone a dramatic transformation over the last 30 days, transitioning from a range-bound environment in early February to a high-volatility "crisis" regime by late March 2026. Following a period where Crude hovered near the $65 level, prices staged one of the most significant rallies in recent history, peaking near the $119–$120 mark in early March. This surge was characterized by a rapid repricing of geopolitical risk as the conflict in the Middle East led to the effective closure of the Strait of Hormuz. However, the price action has recently entered a corrective and highly erratic phase; after testing the psychological $100 resistance last week, WTI experienced a sharp double-digit percentage plunge on March 23 following headlines regarding a potential five-day strike postponement and diplomatic overtures.

Fundamentally, the market is caught in a "binary" setup between a massive structural supply surplus and a localized physical shortage. In February, reports from the IEA and OPEC+ highlighted soft demand and a projected surplus of nearly 1 million barrels per day for the year. This bearish backdrop was abruptly upended by military escalations that shut in an estimated 8 to 10 million barrels per day of regional production due to transit and storage constraints. Currently, the narrative is shifting toward the efficacy of global policy interventions, including the IEA's record 400-million-barrel emergency reserve release. Traders are now weighing whether these strategic buffers and the potential for a diplomatic breakthrough can offset the loss of roughly 20% of global oil flows, or if the market is settling into a structurally higher price floor.

If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs tradingview.com/cme/

*CME Group futures are not suitable for all investors and involve the risk of loss. Copyright © 2023 CME Group Inc.

**All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Oil at Key Support – Bounce Toward 100 or Breakdown ?Price remains in a well-structured ascending Pitchfork, with a clean bullish sequence of higher highs and higher lows.

Following the recent impulsive leg, price is now pulling back into the lower boundary, which is acting as dynamic support.

What stands out:

Clear reaction at Pitchfork support

Bullish structure still intact

Median Line continues to act as a natural draw for price

Macro note:

Ongoing US–Iran tensions are keeping a bid under oil. With supply-side risks in play, especially around the Strait of Hormuz, downside pressure remains limited for now.

Outlook:

As long as the lower boundary holds, a move back toward:

100 (Median Line)

109 (Upper boundary)

remains the favored path.

A sustained bounce could accelerate given the current geopolitical backdrop.

Invalidation:

A confirmed break below support would weaken the structure and open the door for a deeper pullback, though this is not the primary scenario at the moment.

Approach:

No rush on entries — waiting for clear confirmation:

Rejection from support

Or breakdown and retest

Price tends to gravitate back toward the median line.

//What’s your bias here — continuation to 100+ or breakdown from this zone ??

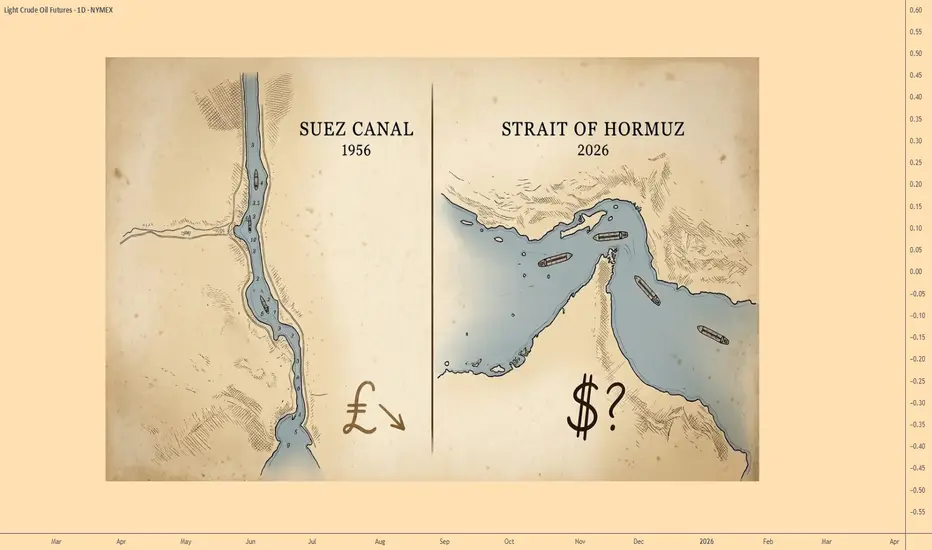

The Dollar's Suez MomentHi and happy start of the new trading week – which will probably be quite eventful!

Most traders watching oil and yields right now are asking the right question — what does this mean for my positions? Fewer are asking the deeper one: what does this mean for the dollar itself?

The Iran conflict isn't just a Middle East story. It's a stress test for an arrangement that has quietly underpinned the dollar's global dominance for half a century. And the results so far don't look great for the US.

The deal behind the dollar

After the collapse of the gold standard in 1971, the US faced a problem. The dollar had lost its anchor. The US administration needed a new one.

The solution emerged from a simple observation: the world runs on oil, and oil needed a pricing currency. Through a series of agreements in 1973 and 1974, the US and Saudi Arabia built what became known as the petrodollar system. The mechanics were straightforward. Oil would be priced and traded in dollars. The US would provide military protection and political guarantees to Saudi Arabia and the Gulf states. In return, the surplus oil revenues — petrodollars — would be recycled back into US Treasury bonds and dollar-denominated assets.

It wasn't a single signed contract. It was a strategic understanding — historians still debate how formal the arrangement ever was, but the outcome was the same regardless of the paperwork. And it worked extraordinarily well for both parties.

The consequences for the global financial system were enormous. Every country that needed to buy oil needed dollars first. That created permanent, structural demand for the dollar from every economy on earth. Central banks accumulated dollar reserves. Dollar-denominated debt became the standard. And the US could run deficits that would have broken any other country — because there was always a buyer for its debt.

This is what economists call the "exorbitant privilege." The US gets to live beyond its means because the world has no choice but to fund it. The petrodollar arrangement is where that privilege was born.

What the deal required the US to deliver

The arrangement had an implicit promise from the US side: security. Not just words, but credible military deterrence in the Gulf. The whole logic only holds if other powers believe the US will act when the infrastructure is threatened.

For decades that credibility held. During the Iran-Iraq tanker wars of the 1980s, the US Navy escorted Kuwaiti oil tankers through the Gulf under Operation Earnest Will — a direct demonstration that Washington would protect the free flow of energy when the arrangement demanded it.

That belief has since been tested again, and more recently it has started to crack.

In September 2019, Iranian-made drones and cruise missiles struck the Abqaiq and Khurais facilities — the largest and most critical oil processing infrastructure in Saudi Arabia. The attack knocked out over 5 million barrels per day of Saudi production overnight, the largest single outage in the modern history of oil. The Aramco CEO publicly stated that an absence of international resolve was emboldening the attackers. Trump tweeted that the US was "locked and loaded." No retaliatory military response followed.

The infrastructure was repaired. The incident was absorbed. But a signal had been sent to every government watching: the US umbrella has gaps.

A waterway that changes everything

The current Iran conflict raises the stakes considerably. The Strait of Hormuz is the single most important chokepoint in global energy markets — roughly 20% of the world's daily oil consumption passes through it, along with around 20% of global LNG trade and significant volumes of other commodities including fertilizers and helium. Oil is the focus here, but the broader point is this: Hormuz is not a niche waterway.

Closing it, even temporarily, would send shockwaves through every oil-dependent economy on earth. Unlike a drone strike on processing facilities, a Hormuz closure cannot be quietly repaired. It requires a military response or a negotiated reopening. Every day it stays closed, the question echoes louder: can the US project sufficient force to reopen it? Will it?

Trump called on allies across Europe and Asia — and even China — to send warships. No country publicly committed.

This happened once before

The pattern is not new. Seventy years ago, Britain faced a strikingly similar moment.

In 1956, Egypt's President Nasser nationalised the Suez Canal. Britain and France, with Israel, launched a military operation to retake it. Militarily, the operation succeeded quickly. Then the US stepped in — not to help its ally, but to end it. Eisenhower threatened to sell US holdings of British pounds, flooding the currency market and forcing a devaluation. He blocked IMF loans. He refused to supply oil unless Britain accepted a ceasefire. The US Treasury Secretary told his British counterpart directly: there would be no American money until British troops were out of Egypt.

Britain withdrew. The pound sterling was the world's second reserve currency in long decline — Suez finished the question. Countries across the sterling area began converting their pound holdings into dollars. The process that had been gradual became irreversible. Britain's era as a global power ended not on a battlefield but in a currency market. The lesson drawn by historians was simple: the moment a power can no longer assert its will over a strategic waterway, it removes any remaining doubt about the financial architecture built on that power.

Seventy years later, the US finds itself in a very similar position to the one Britain was in 1956. A strategic waterway. A challenged ability to project force. Allies who didn't show up. To be fair, the parallel has limits — the US enters this moment from a position of considerably greater financial and military depth than Britain had in 1956. The dollar's institutional advantages are not Britain's thin reserve position. But the structural similarities are hard to ignore.

The process that's already underway

Here is the important caveat, and it matters: de-dollarization is not a sudden event. It is a slow, structural process. Anyone waiting for a single announcement that the dollar is finished will wait forever.

Ray Dalio has been writing about this transition for years — the historical cycle of reserve currencies and the shift toward a multipolar financial world. When he was writing about it, few outside specialist circles were paying attention. The broader conversation only entered mainstream awareness more recently — most visibly when Canada's Prime Minister referenced it at Davos earlier this year, which prompted a wave of political leaders to claim they had always understood that old world order is not working anymore. That's how these things work. The process moves slowly, then suddenly it's in the room.

But the data was already there for those looking. Central banks worldwide have been quietly reducing their dollar reserves and buying gold at the fastest pace since the 1950s — three consecutive years above 1,000 tonnes annually. Some BRICS nations have been exploring alternatives for trade settlement. China and Russia have been conducting bilateral energy deals in local currencies.

The EU dimension is perhaps the least discussed — and arguably the most significant. The EU is the world's largest energy importer. It has historically priced that energy in dollars, in part because the US military umbrella over the Gulf made dollar-denominated energy the path of least resistance. Worth noting: Europe isn't the main buyer of Gulf oil by volume — Asia is, receiving roughly 85% of Hormuz crude flows. But the dollar pricing question is separate from the physical flow question, and it's on the pricing side where Europe's weight is felt.

The current US administration has pushed Europe toward full strategic autonomy (although it prefers to see Europe divided)— on defense, on energy, on trade. If Europe no longer needs or receives that military umbrella, the incentive to price energy in dollars weakens accordingly. An autonomous Europe buying the world's largest volume of energy on its own terms has no structural reason to insist on dollar settlement. The US could threaten tariffs in response — and likely would — but that's a negotiation, not a veto. The compliance was always optional — that was simply the arrangement between good allies.

None of this means the dollar collapses. The dollar's advantages — deep liquid markets, legal infrastructure, institutional inertia — are enormous. But there is a difference between the dollar remaining important and the dollar maintaining its monopoly. The exorbitant privilege lives in the gap between those two things.

What this means for markets

For traders watching these dynamics, a few markets are more directly exposed than others.

Dollar pairs such as EUR/USD are the most direct read on dollar status over time — though in the short term, crisis conditions often paradoxically strengthen the dollar as a safe haven.

Gold — the traditional alternative reserve asset. Central bank accumulation is already visible in the data and has been running at historically elevated levels for three years. Gold doesn't need the dollar to fail for it to benefit — it only needs the dollar's monopoly to weaken.

US 10-year yields — if foreign demand for US Treasuries softens, yields need to rise to attract buyers. Longer-term structural question is who finances US debt if petrodollar recycling slows.

Oil — the most direct exposure to the Hormuz situation. The near-term volatility is obvious. Interesting question is what happens to oil pricing mechanisms if the petrodollar arrangement continues to erode.

If the US succeeds in projecting sufficient force and the Hormuz situation resolves, some of this reverses in the short term. The dollar might rally. Yields might pull back. Oil might settle. But the structural process doesn't reverse with it. Britain "won" militarily at Suez in 1956 too. That didn't change what followed.

We may be watching a Suez moment for the dollar. Not the end of something — the beginning of a long transition.

Thank you and enjoy your trading!

Crude — What Happens If Hormuz Stays ClosedSunday's analysis made the bearish case for crude at $98.23 — record speculative crowding, producer hedging at $100+, and structural oversupply once Hormuz normalises. The confluence was strong across four of five disciplines. But the word "normalises" is doing heavy lifting in that thesis — so here is the bull case that challenges it.

The Case Against

The Iran conflict has now entered week four of active Strait of Hormuz disruption — significantly longer than the typical 7-14 day Middle East risk premium fade pattern that the bearish thesis relies on. Iraq has declared force majeure, Kuwait refineries have been attacked, and the theatre appears to be expanding rather than contracting. The IEA has confirmed 8 mb/d curtailed — the largest supply disruption in oil market history. The U.S. policy response of releasing sanctioned Iranian cargoes and SPR volumes may prove insufficient if the disruption extends beyond Q2. Qatar's $150/bbl scenario and Goldman's own revised forecast acknowledging longer disruption expectations suggest the tail risk is not trivial. Most critically, the bearish thesis assumes geopolitical premium fade within 3-4 weeks — but this conflict shows no signs of de-escalation, and the historical precedent for this scale of Hormuz disruption simply does not exist.

The Trigger to Watch

The critical level is $100 on a weekly close basis. A sustained break above psychological resistance would signal the market is repricing for extended disruption rather than normalisation, opening a retest of the $110-120 March spike zone. Watch for any headlines indicating expanded military operations, additional force majeure declarations, or failure of U.S. SPR releases to offset curtailed Hormuz flows.

Net Assessment

The primary bearish thesis remains stronger than the contrarian case. The weight of structural evidence — IEA demand downgrades, OPEC+ production increases, and extreme speculative crowding — favours mean reversion once the disruption fades. The contrarian risk is real but relies on a specific geopolitical outcome (sustained escalation) overriding fundamental market dynamics. The thesis holds unless $100 breaks on a weekly closing basis.

Crude Oil Technical Position: BullishCrude Oil is at resistance, but given how clean the reaction to the upside was, I expect it to break.

Elliott Wave Outlook: Oil (CL) Zigzag Rally Targets $110 AreaAfter surging to $119.7 on March 9, crude oil experienced a sharp decline, reaching $76.73 by March 11. This retreat unfolded in the form of a five-wave impulsive Elliott Wave structure, marking a decisive corrective phase. From the March 9 peak, wave (1) concluded at $96.25, followed by a rebound in wave (2) that terminated at $104.57. The subsequent decline in wave (3) reached $81.19, while wave (4) produced a modest recovery to $91.48. The final leg, wave (5), extended lower to $76.73, thereby completing wave ((A)) at a higher degree.

Currently, a corrective rally in wave ((B)) is underway, developing internally as a zigzag formation. From the termination of wave ((A)), the initial advance in wave (A) ended at $102.44. A subsequent pullback in wave (B) found support at $84.37. The ongoing rise in wave (C) carries potential to extend further, targeting the 100% to 123.6% Fibonacci extension of wave (A). This critical zone lies between $110.3 and $116.5, where renewed selling pressure may emerge. Should sellers reassert control in this region, oil prices could resume their decline in wave ((C)), provided the pivot at the $119.7 high remains intact.

Bullish Divergence & Demand Zone Hold – Eyeing a Return to 104Despite today’s -0.19% dip to 100.79, price is holding firmly above the 100.00 psychological level.

Here’s why I’m turning bullish:

1. Hidden Bullish Divergence (MACD)

Price made higher lows, but MACD histogram printed a higher low as well – signaling underlying momentum shifting up.

2. Demand Zone Intact

The 100.76 low matches previous support from mid-March. Buyers are defending this area.

3. Rejection of Lower Prices

Wicks below 100.80 got bought up quickly. No close below 100.50.

4. Target

First resistance at 102.00, then 104.00 (mid-April highs).

Invalidation:

A daily close below 99.50 would cancel this bullish view.

Options Blueprint [Adv]: Financing a Convex Asymmetric HedgeMarket Context

The setup on the chart is not just about momentum. It is about what happens when a market clears an important prior high through a gap and then starts trading in a region where overhead resistance becomes more widely spaced.

Here, price opened above the prior March 16, 2026 high at 102.44. That matters because a gap through a prior high can signal a regime shift: the market is no longer negotiating the old range, it is testing whether buyers are willing to accept higher value. In this case, the weekly gap itself may act as support if the breakout is genuine.

The backdrop also helps explain why the market is paying attention to upside risk. Reuters reported on March 30 that Oil was heading for a record monthly rise and U.S. WTI was trading around 102.56 as the conflict involving Iran widened and disruptions expanded beyond the Strait of Hormuz into other key energy chokepoints. Reuters also noted that Barclays sees a prolonged Hormuz disruption as potentially removing 13–14 million barrels per day from global supply, roughly one-fifth of world oil and LNG flows moving through the strait. AP separately reported that attacks on regional energy infrastructure and restrictions tied to the strait have kept pressure on oil markets elevated.

That does not mean price must keep rising. It means the market has a plausible catalyst for upside expansion, which is exactly the type of environment where hedging upside exposure can become relevant.

Technical Landscape

Once price moved above 102.44, the chart opened a path toward a set of higher resistance references:

119.48 from March 2026

123.68 from June 2022

130.50 from March 2022

147.27 from the July 2008 high

The important detail is not simply that resistance exists. It is that these levels sit meaningfully above the breakout area. If acceptance above the gap continues, there is room for an expansion move before the market encounters the next major technical barriers.

Below price, the chart shows a relevant UnFilled Orders support area near 91.73 down to 86.46. That zone matters because it helps define the logic of the hedge. If price holds above the breakout and the weekly gap remains supportive, the upside thesis stays alive. If price breaks down through that support structure, the market may be signaling a different regime altogether, and the need for upside hedging becomes less urgent.

Why Use a Hedge Here Instead of Chasing Price?

Breakout markets often tempt traders into late directional entries. The problem is that a strong move can already be carrying elevated implied volatility, emotional urgency, and poor location for a simple long entry.

A hedge solves a different problem. It is not trying to squeeze every dollar out of the move from current levels. It is trying to create protection or upside participation if the market starts stretching into the higher resistance zones. In other words, the concern is not the move from 102 to 106. The concern is what happens if the market starts pressing toward 119.48 or beyond.

That is where a convex structure becomes interesting. Rather than paying outright for a long call, the structure uses premium collected from a bullish put spread below price to help finance a higher-strike call above price.

The Structure

The strategy shown on the chart is:

Sell the 100.5 put

Buy the 90 put

Buy the 119.5 call

At the time of the screenshot, the full structure could be entered for a net credit of 0.12 points.

This creates a defined-risk, convex payoff profile:

The short 100.5 / long 90 put spread collects premium below price.

That premium helps finance the long 119.5 call.

The result is a structure that does not need a large move immediately, but becomes much more responsive if price starts accelerating into the upper resistance zones.

This is why the idea is asymmetric. Downside risk is capped. Upside remains open above the long call strike.

Payoff Logic

The maximum loss is 10.38 points, which comes from the width of the put spread (10.5) minus the 0.12 credit received.

The lower breakeven on the put spread side is 100.38. Above that level at expiration, the short put spread side is no longer losing money. Above 119.5, the long call starts adding intrinsic value on top of the original credit.

That means the structure has two very different personalities:

Between 100.38 and 119.5, the structure is mostly about preserving the initial credit and avoiding damage on the put spread side.

Above 119.5, the profile starts to become more dynamic because the call begins participating in further upside.

That distinction is important. This is not a structure designed to monetize a modest drift higher. It is designed for a market that could stay firm and then transition into extension. The structure gets better as the move gets larger. That is the essence of convexity.

Trade Idea and Scenario Plan

As a case study, the entry logic centers on the market holding above the breakout gap and continuing to accept value above 102.44.

A practical scenario framework could look like this:

Entry zone: while price remains accepted above the breakout level near 102.44 and the weekly gap remains constructive

First technical objective: 119.48

Secondary objectives: 123.68, then 130.50

Invalidation zone: a meaningful loss of the UnFilled Orders support area around 91.73 to 86.46

Defined risk: 10.38 at expiration, with the worst-case payoff reached below 90

From a trade management perspective, a hedger may not need to wait for expiration if the market clearly loses the support structure. If price starts closing back inside the old range and then breaks the 91.73 area, the original rationale for upside protection weakens materially.

Because the long call sits at 119.5, this setup is explicitly saying: “I do not need much between here and there. I need the structure to wake up if the market starts pressing into the higher resistance band.”

Contract Specs: Standard and Micro

For the standard NYMEX contract, the WTI crude oil futures contract minimum price fluctuation is 0.01 per barrel, or $10 per contract.

For the Micro WTI crude oil futures contract, its minimum price fluctuation is 0.01 per barrel, or $1 per contract.

That distinction matters. The standard contract offers larger notional exposure, while the micro contract allows much finer sizing. For traders and hedgers who want to scale exposure more precisely, MCL can make structure-building more flexible simply because each tick carries one-tenth of the dollar impact of CL. Contract design details are set by CME; position sizing and suitability remain individual decisions.

The futures margin figures to be kept in mind are ~$11,000 for CL, versus about ~$1,100 for MCL. Margin figures change over time, so these should be treated as time-sensitive reference points rather than static numbers.

Risk Management

The most important feature of this structure is not the call. It is the discipline built around the downside.

Because the long 119.5 call is financed by a short put spread, the trade is not “free.” It carries a clearly defined maximum loss of 10.38. That means position sizing has to begin there, not with the small credit received and not with the hope of a larger move.

A useful way to think about the risk is this:

If the breakout holds, the structure can remain aligned with the chart.

If price collapses through the support structure and into the lower put strike region, the market is likely no longer in the scenario this hedge was designed for.

That is why technical invalidation and risk sizing have to work together.

Defined risk does not eliminate risk. It makes the risk measurable.

Closing Thought

This is the kind of options structure that makes the most sense when the chart and the macro backdrop are speaking the same language. The chart shows a gap through a prior high and relatively open space toward the next resistance zones. The news backdrop shows why the market is paying attention to upside supply risk in the first place. Together, they create an environment where a convex asymmetric hedge can be more logical than simply chasing a breakout.

The structure is also honest about what it wants. It is not trying to monetize every inch of the move. It is trying to be in place if the market starts doing something bigger.

Data Consideration

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

USOIL: Bearish Engulfing with Bearish Divergence Targeting $66As stated in the descriptions previous ideas I have included in the related publications oil was likely to significantly spike up but then pull back significantly below $100 for at least a week or so as the indexes staged a recovery. So far we have seen a spike up reaching as high as $119 per barrel or $2.84 per gallon and we have seen a decline and stagnation around the $100 per barrel or $2.40 per gallon mark all the way down to as low as $77BLL or $1.84GLL, but we have since rallied back to the $100 zone. However, at this level we have seen Oil Bearishly Engulf on the Daily Timeframe and have seen Bearish Divergence in the RSI. I think it is likely that oil will have to see an even greater pullback towards the 200-day EMA in white currently at around $66 per barrel and $1.56 per gallon and fill the unfilled gap. After coming down to test the 200 EMA and filling the gap at $66 I think oil could very well continue higher reaching as high as $178 per barrel but that's a long time from now.

Previous Bullish Oil trade listed in the description of this idea .

Most recent call for Index recovery and for Oil to come back down well below $100 listed here.

Strange Observation with CRUDE TrendlinesI did the TA so you don't have to :)

Current price pop was "ALSO" a break of older downward trend line from 2022.

We are trending up at a steep angle 5 only. if we retrace down, will look for support around and between angle 4 & 5 (UP)

What do you see ?

Light Crudeoil Futures hourly analysis for the week till Mar 28I have a bullish view on Light Crude Oil Futures during the week. It may take support

at 94.20 and may bounce back with the targets of 103.47 and 104.50 during the week.

This is my personal view as my Market Timing Analysis. Please use your own technical study for real-time trading with proper risk management.

Will Brent Crude Oil Stabilize?Well, Iran apologizing to neighbors and this right at a previous trader emotional decision making behavior area (around March 2023). Is this coincident or will it break the resistance?

Share your thoughts.

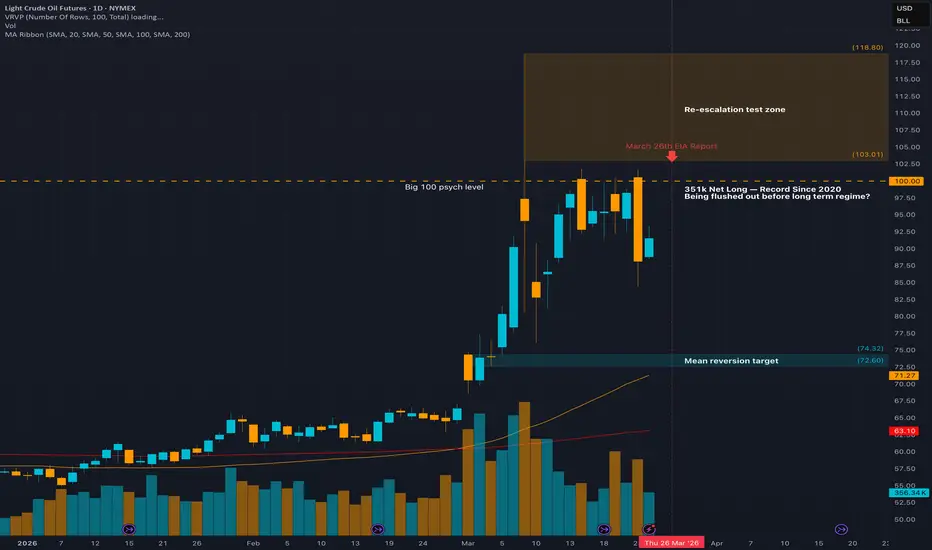

Crude — Specs vs Producers: Who's Right at $100?The Commitment of Traders data for crude oil reveals one of the most extreme positioning divergences in recent history. Managed money — hedge funds and speculative traders — has piled into the most bullish net-long position since 2020 at 351,032 contracts. At the same time, producers are aggressively hedging at $100+ levels. When these two groups disagree this violently, one of them is wrong.

What the Data Shows

COT data decomposes market positioning by participant type. Managed money represents speculative capital — trend followers, macro funds, and momentum-driven traders who are typically late to crowded moves. Producers represent commercial hedgers — the companies that extract, refine, and sell physical crude. Their hedging decisions reflect forward-looking views on sustainable prices based on actual cost structures and physical supply-demand. Nearly 25% of AEGIS hedging clients are actively locking in forward sales at $100+, the highest hedging activity in years. This behaviour pattern signals that the people who sell oil for a living view current prices as unsustainably high — a selling opportunity they may not see again soon.

Why It Matters for Crude

Record speculative longs create mechanical downside risk. Every net-long contract is a future sell order. When price stalls at resistance — as it did at $100 on March 20 — the crowd holding record long exposure faces a choice: wait for a breakout that may never come, or liquidate into a falling market. Producer hedging at these levels adds structural selling pressure from above. The $98.23 current price sits in a zone where speculative longs are underwater on recent entries while producers are actively selling forward, creating an asymmetric setup where downside flows outweigh upside demand.

What to Watch

The next COT release covering the week ending March 24 is the key data point. If speculative longs remain near 351k or increase despite price consolidating below $100, the crowding risk intensifies. If significant liquidation appears — net-longs dropping below 300k — the unwind has begun and mean reversion toward $70-75 accelerates. That single data release clarifies whether the crowd is holding conviction or starting to exit.

CRUDE OIL - short set upCRUDE OIL - short set up

Hi Traders,

this is not an easy trade but had a good odds; but it is only for expert. You must have a good money managment to do that.

From my point of view the price area from 110$ to 93$ is a sellingarea; my idea is open a several trade with small size in this area; this will be a distribution of trade in the time. I will covered with call option so in case of a big long spike (up 120$) my loss will be covered by option prize so be carefull if you want follow this strategy.

Crude — Record Longs Meet Producer Hedging at $100WTI crude sits at $98.23 after rallying from $67 to $119.48 in one of the largest weekly moves in 43-year futures history — triggered by the Iran-U.S. Strait of Hormuz disruption. But as the conflict enters week four, speculative positioning has reached its most bullish level since 2020 while producers are aggressively locking in forward sales above $100. That divergence between speculative conviction and commercial hedging behaviour is the setup.

Directional bias: BEARISH | Confidence: 6/10 | Timeframe: Next 2-4 weeks

The Setup

Managed money net-long positions surged to 351,032 contracts as of March 10 — the most bullish speculative positioning since 2020, representing a historical peak in crowd conviction. Simultaneously, nearly 25% of AEGIS hedging clients are actively locking in forward sales at $100+ levels, signalling that the commercial participants who understand physical market dynamics see current prices as a selling opportunity. This creates a classic pain-trade configuration: maximum speculative length at price peaks while smart money sells forward. The technical picture confirms distribution — WTI was sharply rejected at $100 psychological resistance on March 20, and a bearish symmetrical triangle breakdown pattern is forming within the $94-98 consolidation range.

Key Levels

Resistance 2 (Major): $119.48 — March spike high, geopolitical panic peak

Resistance 1: $100 — Psychological resistance, March 20 rejection level

Current Price: $98.23

Support 1: $92 — Immediate support, triangle breakdown trigger

Support 2 (Major): $85 — Deeper structural support if geopolitical premium fully fades

Confluence Check

📊 Technical: Consolidating $94-98 below $100 resistance with bearish triangle breakdown forming after March 20 rejection — CONFIRMS

📈 Fundamental: IEA projects 1.9 mb/d global surplus once Hormuz normalises, demand growth cut 210 kb/d to 640 kb/d; crude overvalued 15-20% versus $60-70 fair value — CONFIRMS

🏛️ Institutional: Record speculative net-long 351,032 contracts versus producer hedging surge at $100+ creates asymmetric downside — CONFIRMS

⚡ Options/Vol: Elevated implied vol but neutral put/call positioning reflecting uncertainty rather than directional conviction — NEUTRAL

🌐 Economic: ISM Manufacturing 52.6 shows expansion but China GDP 4.5% dampens global demand outlook; Fed on hold adds macro headwind — CONFIRMS

Risk & Invalidation

The primary risk is sustained Iran conflict escalation beyond current containment. A prolonged Strait of Hormuz closure disrupting 1-2+ mb/d flows could force Goldman Sachs' bull-case $150/bbl scenario. Probability is assessed as low given the U.S. has announced plans to release sanctioned Iranian crude cargoes and SPR volumes specifically to counter the disruption. The thesis is invalidated on a weekly close above $100 — a failure to reject this level would signal the geopolitical premium is re-accelerating rather than fading.

Catalyst & Timing

The EIA Weekly Petroleum Status Report on March 26 is the next data point for validating whether inventory trends confirm the structural oversupply thesis. The mean reversion setup targets $70-75 as the geopolitical premium fades over the next 2-4 weeks, consistent with historical patterns showing markets dismiss Middle East risk premiums once the initial shock is absorbed. Goldman Sachs' own revised Q4 2026 forecast of $67-71 implies 28% downside from current levels even with extended disruption assumptions.

Lucky cement psx. CORRELATION WITH OIL PRICEIn this chart you can see the correlation between oil prices( upper panel) and share price of lucky cement( lower panel) if oil prices retain between $120 and $ 135 for a period of 3 to 4 months then you will see lucky cement share price touching 200 rupees.

Note* the oil price has already touched 119.48 but it was retraced back to 70s and now standing at $96 ( US benchmark) and price of brent crude oil ( uk benchmark)is $110

The price of US benchmark is low because US is a net exporter of oil.

CL going for GAP closedue yesterday movement that weren't able to close above 59.64 , we will go lower today closing the gap.

a good 70p from here.

Crude ready for next jump 10200,11300Crude cup and handle pattern ready for next target.

Neck line 9200-9300

Wait for breakout

CRUDE OIL STILL BULLISH BUT MIGHT PULLBACK TO BUYZONE! Hey Traders as mentioned on my Channel During The Sunday Night Futures Market watching the support levels on Crude Oil. These are the Demand Zones you want to watch as the market might test them moving forward.

Bullish- Yes I am so the war is causing alot of price spikes and it looks to continue at least for now and possibly longer term. Remember in the past crude went up to almost $150 Barrel during last Crisis in 2008. But I think we need a pullback to the buyzone back to support. Don't chase the rally let it come to you.

Bearish- uhhh well I guess if they announce a deal that sends a shockwave through the markets then yes. But for me to become Bearish I think I would have to see the market close below signficant support. If we get daily close below 86.00 then yes I will start to become Bearish.

Commitment of Traders- Showing strong institutional buying right now that large Speculators are holding over 200,000 contract long. So usually that is a sign that the trend will continue but we have to wait and see this Fridays report to see if they open more long positions or possibly start to close some.

Good Luck & Always use Risk Management!

(Just in we are wrong in our analysis most experts recommend never to risk more than 2% of your account equity on any given trade.)

Hope This Helps Your Trading 😃

Clifford

RISK DISCLOSURE

TRADING IN THE FUTURES AND FOREX MARKET INVOLVES SIGNIFICANT RISK. ALWAYS CONSULT A FINANCIAL ADVISOR AS HIGH RISK ASSET CLASSES MAY NOT BE SUITABLE FOR ALL INVESTORS. THIS IS NOT A RECOMMENDATION TO BUY OR SELL ANY ASSETS. ALL IDEAS ARE MADE FOR EDUCATIONAL PURPOSES. PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING.